Investor Alert: Is Masterworks.io a scam?

Every once in a while, someone decides to sell shares in “something” new. Today, that something is Fine Art. Let’s explore the pitfalls of investing in this idea.

Investing in Art

Purchasing art has always been about buying a single piece of artwork outright. Meaning, you find a piece of art you like and you buy it. That means that piece of art is yours to display in any way you wish. This type of purchasing of art is (and remains) the most optimal way to purchase art. You buy it outright and you own the entire work in totality.

However, there are exceptions to the above. If you purchase a reproduction of an original work of art, this purchase offers much fewer rights to the buyer. Some rights that you forfeit when purchasing a reproduction include reproduction of that art. Meaning, you can display your purchase in any way you choose, but you cannot photograph it and/or sell photographs of that art. The reproduction rights remain with the original work’s owner. Only the person who owns the original artwork may reproduce the work in any way.

Mass Produced

You may be thinking, “But, mine is painted with real paint on real canvas”. That doesn’t matter. What matters is if the painting is the first and the original. Many painters reproduce their works using paint on canvas, many times over. Typically, these reproduction paintings are painted by employees (in a sort of paint-by-number situation), but is not always painted by the original artist. These are painters hired for the sole purpose of creating a copy of the original. These reproduction paintings are sold typically at a fraction of the original art’s cost. These reproductions rarely become valuable simply because of the total number produced. It’s the same reason why many mass produced items rarely go up in value.

Because the original was painted by the actual artist, this original painting is the one that holds value. That’s not to say that every original painting by every artist will increase in value. Many do not. It depends on the artist, the artwork and that artist’s contribution to the art world. Perhaps in time that artist might be seen in some kind of historical light, thus propelling their artwork values upward.

Because an original art piece might spawn many “authorized” copies, copies that could become very popular in sales, that makes the original work much more valuable. For example, an original Thomas Kinkade painting would be worth far more than one of its many reproductions. That doesn’t mean reproductions can’t increase in value, but they will never be valued the same as the original first painting.

Masterworks.io

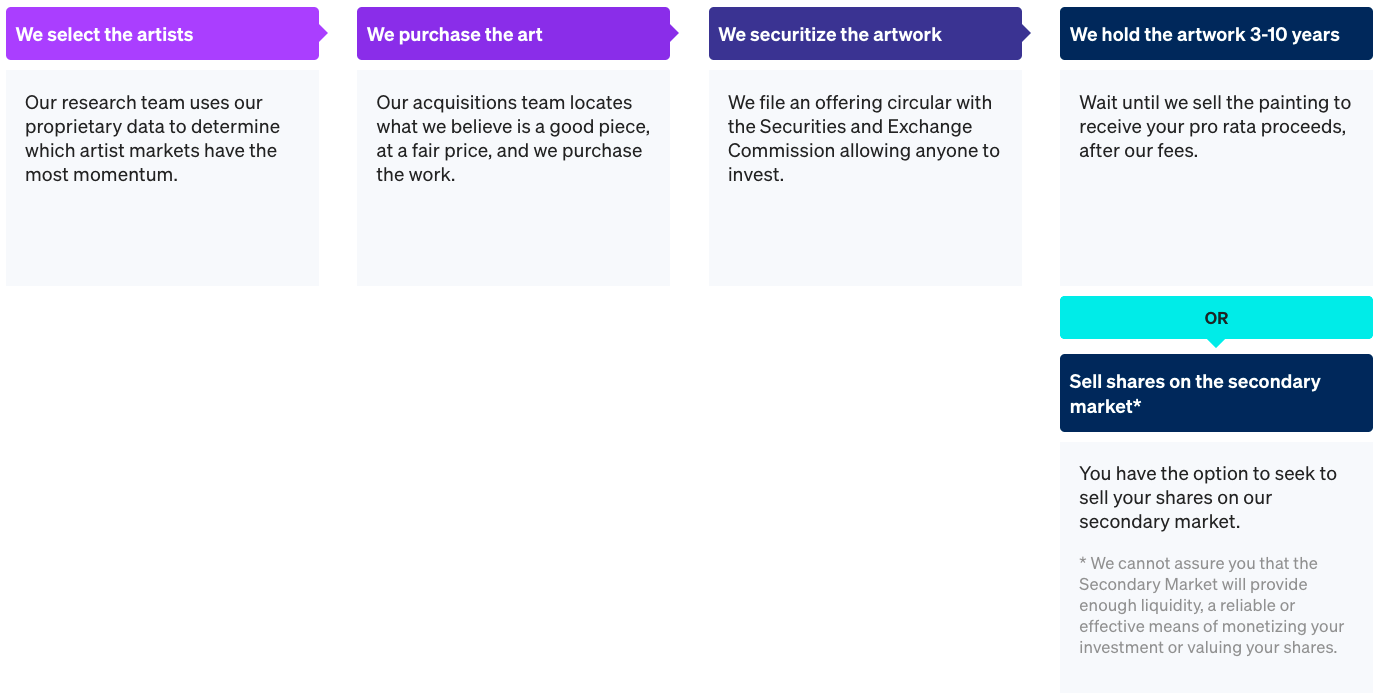

Masterworks takes the idea of Fine Art to an “investment” level. By that I mean instead of owning the actual painting / art piece in full, you only own a “share” (or small portion) of the art. In reality, this type of investing is an abstract concept. At the moment, Masterworks appears to focus solely on paintings. You might be wondering, “How does owning a small piece of a whole actually work?”

The short answer to this question is that it doesn’t. Investing in a tiny piece of a valuable work of art doesn’t do anything but ultimately make Masterworks as a company rich. You, in fact, don’t own anything but the knowledge that you “might” own a small piece of a work of art. You also own the knowledge that that investment might, maybe return value IF the painting is (eventually or ever) sold at a profit. In essence, you’re essentially placing a long shot bet that eventually that painting might be sold for a profit.

Let’s understand some of the problems with this idea.

Where is that painting?

Good question. If you’re buying into an investment object, you definitely want / need to know exactly where that “object” is physically located in the world. If you invest in a company, for example, you know where their headquarters are. You know who their executives are. You know their physical address and phone number. You can call and talk to someone. You can even find out their sales plans, the products or services the company sells and how much they make in revenue per quarter. Keep in mind that some private companies may be unwilling to disclose their sales numbers. With public companies, that company’s revenues are public knowledge.

Buying into a Masterworks painting, on the other hand, you don’t know exactly where it is. You don’t know under what conditions it’s being stored. You don’t know who currently has possession of it. Masterworks can “assure” you that that item is safe… but is it? Paintings are particularly susceptible to deterioration if not kept under the strictest of environmental controls. Artwork is also susceptible to theft. Both of these issues are difficult to manage at the best of times.

One might think that paying to invest in small bit of a painting might help protect it from being lost to time. It’s a lofty ideal. It’s, unfortunately, an ideal that when considering the underlying logistics of it all, make the investment seem highly risky. It’s also an ideal that may not hold true.

An investor should always ask, “Who owns the original work?” You must also consider the following:

- Is Masterworks attempting to sell shares in art they don’t legally own?

- Is Masterworks actually in possession of the art they claim to have bought?

- Did Masterworks actually buy the painting or is it under some kind of “lease”?

- Is the art being stored in correct conditions?

Who knows for sure? These are all very good questions. They’re also questions that should greatly concern you when considering “investing” in art through Masterworks.

Paintings as Investments

Art is entirely subjective to every person, but it is also highly volatile in its salability. What I mean is that paintings, particularly abstract paintings, go through ebbs and flows, waxing and waning in popularity and, yes, value. What might seem like an excellent painting today may be seen as outdated and worthless next year. Art’s value comes and goes, sometimes as a result of changing style trends. Painting values are, as I’ve said above, highly volatile. Way more volatile than investing in company stocks, bonds or even precious metals.

Sure, this investment type is yet another “thing” you can put some money into as part of your larger investment portfolio and hope to see a return on investment, but it may not return anything. The problematic issue with this concept is, can Masterworks be trusted or are they simply another Bernie Madoff? This is the ultimate question.

Novel Concept, Poorly Realized

The idea of share investing in art is definitely novel, even Masterworks states as much. However, is it realistic?

First, there’s the idea that you only own a tiny fraction of a painting. How does that work anyway? Are they planning on cutting up the piece of art if the art price bottoms out and there’s nothing left to pay you back your investment? Clearly, no. They’re simply going to tell you that you’re out your money and they STILL get to keep that art even if it’s worthless. Not only do you NOT get the art after investing, you don’t get your investment back if the painting is sold at a loss.

Second, there’s the logistics of where this art is stored. You have no idea as an investor. Unless Masterworks intends to spend boatloads to create a location to store all of this art under perfect archival environmental conditions (highly unlikely) AND they can prove that fact to investors, the art is then completely open to deterioration, decay and possibly destruction or even theft. Some art, in fact, may be produced using non-archival media. This means that no matter how well a piece of art is stored, it may still slowly (or quickly) deteriorate to the point of no longer even being art (or saleable) even within a few months. You can’t stop deterioration, which actually makes some art less valuable every day that passes.

Third, who actually owns (and holds) that art? Are art owners selling the full piece of art, selling it under consignment or are they selling only the concept of ownership as shares, so then Masterworks then manages that “concept trust”? If Masterworks is selling shares in works of art they do not rightfully own and possess, that is very close to a Ponzi scheme. It may also be very illegal. That’s like someone claiming to sell you the Brooklyn Bridge. Sure, anyone can claim to sell it, but they do not own it. They do not even own a piece of it. Giving money to someone claiming to sell you the Brooklyn Bridge is, thus, the very definition of a scam and fraud. With Masterworks, be very careful.

Masterworks needs to also be very careful in what they are doing, making sure their ‘i’s are all dotted and their ‘T’s are all crossed.. Here’s what Masterworks has to say about their own model and art investing:

‣ We have a novel and unproven business model.

https://www.masterworks.io/

‣ Masterworks issuers do not expect to generate revenue, so investors will only recognize a return on their investment if the painting is eventually sold at a profit

‣ No market exists for the shares and paintings are highly illiquid, so you must be prepared to hold your investment for an indefinite period.

‣ Each Issuer owns a single painting and this lack of diversification magnifies risk.

‣ Your ability to trade or sell your shares is highly uncertain.

‣ Paintings may be sold at a loss.

‣ Costs will diminish returns.

‣ Investing in art is subject to numerous risks, including (i) claims with respect to authenticity or provenance, (ii) physical damage, (iii) legal challenges to ownership, (iv) market risks, (v) economic risks and (vi) fraud.

‣ Issuers are totally reliant on Masterworks.

‣ Masterworks has potential conflicts of interest.

‣ Timing of sale of a painting is uncertain.

None of the above (or even their web site) describes how or where the art is actually stored or maintained. It almost solely discusses the risks of investing. The fact that Masterworks also finds the need to call out that purchased shares are “illiquid” says a great deal here. This word means that there are few participants, thus low volume, which ultimately means a very low chance of ever being able to sell out of purchased shares.

Consider stocks and bonds. You can likely sell out of any of these positions in about a day. With Masterworks investments, the low volume and few participants means once you invest, you’re likely stuck holding onto that investment until the painting either sells (at a loss or profit) or fails to sell at all. Masterworks doesn’t really state what happens if you can’t sell your position with a painting that never sells. I guess you’re ultimately out your investment money.

Art Storage

As with any artwork and has been stated above, it’s important to understand how and where the art is stored and who actually owns the art. None of this is explicitly stated on Masterworks’s site. I’m actually taken aback by the fact that for all the deluge of investing information provided, there’s equivalently a severe lack of information regarding the artwork itself, where it’s stored, how it’s managed or who owns it while it’s being held for shares. That’s a big, nay HUGE, problem in my book.

However, Masterworks does say this…

What this ultimately says is that Masterworks locates and purchases art. It doesn’t exactly state what “purchase the work” actually means. Are they taking possession of the work or are they leaving it at the gallery where they found it to remain on sale? They do claim to hold a work of art for 3-10 years. I’m uncertain how this works exactly considering the second half of that “OR” statement. Only questions, few answers.

As I said, for as much information as there is about risk of investing, there’s equally as little about the actual artwork itself… which is huge red flag 🚩.

Any business straddling both the art world and the finance world should be, at once, both engaged in explaining how and where the art is to be stored and handled, but also able to explain the risks of investing. Clearly, Masterworks is only interested in documenting half of this equation.

Volume Investing

Masterworks hopes that as more people jump on board with their share idea and begin investing, a larger and higher volume share marketplace will eventually emerge to allow for easier share trading. At this moment, however, Masterworks has stated that any position you buy is likely to be “illiquid”, thus implying that this is a new market with limited options for selling shares.

In other words, if you invest $100 into a painting and gain 2 shares, those shares in that painting are most likely to remain yours until the painting sells at a profit or a loss. The question is, though, even if the painting sells, does Masterworks have the painting to sell? I’m still skeptical.

Art Galleries

Masterworks, as a company, needs to be a whole lot more forthcoming about all aspects of its business operations, especially surrounding where, how and who stores the art after it’s purchased.

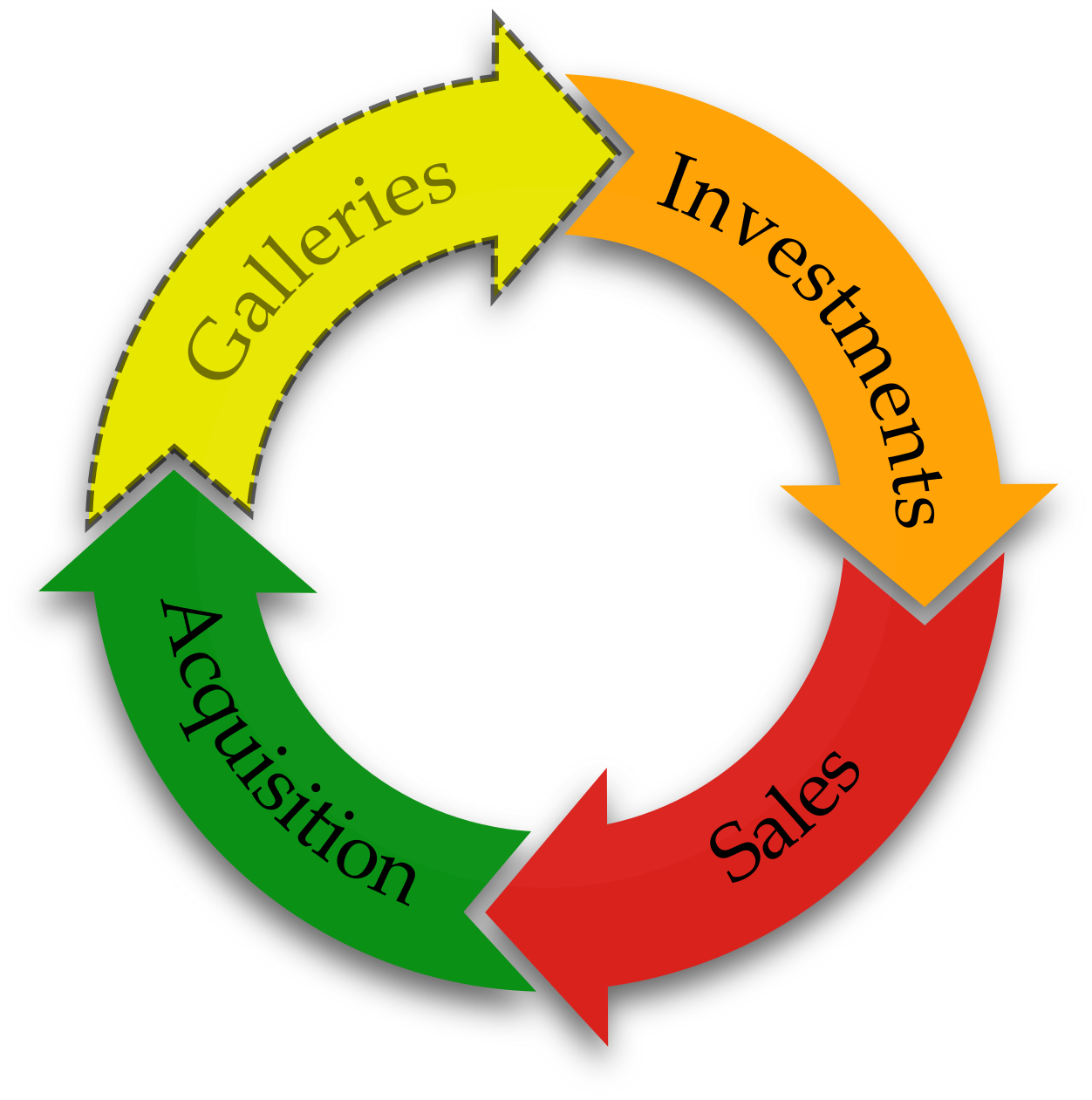

What Masterworks should have planned for is purchasing a number of galleries around the United States (or around the World) to support their business model. Instead of simply attempting to sell the investment share idea, they should have worked this idea full circle.

Here’s where things get a little dicey for Masterworks. Instead of creating a complete sales cycle (or sales funnel as some might call also it), they leave out one very important piece: Galleries. Clearly, they have Acquisition, Investments and Sales. Though, questions about Masterworks’s acquisition process remains, primarily because they don’t have galleries.

To really make this business model complete, Masterworks needs to own and operate its own set of galleries. Why galleries? Owning galleries sets a tone that you know how to properly store and manage expensive artwork in addition to offering a place to actually sell it properly. Though, paintings can be sold through auction houses as well. Masterworks is attempting to sell art for millions of dollars, yet Masterworks doesn’t really state where, or more specifically how, that artwork is managed and stored. It’s an important and necessary piece that’s conveniently missing.

Owning galleries keeps Masterworks honest and allows for auditing. If there is a gallery where a specific investment work lives, investors can visit the gallery and physically see the art they have invested in. This verifies that the artwork exists, that it is genuine (not faked), that it’s in Masterworks’s possession and that it can be verified. Without this piece, verification of the actual art remains an open question. Images on a web site do not verify that anything is genuine. Talking to someone on the phone doesn’t verify authenticity either. Only physically seeing the artwork in person can an investor verify the painting and, thus, verify that their investment is backed by something real.

Questions without Answers

That leaves too many open questions. Questions like, “What exactly am I investing in?” Like, “Where is the artwork stored?” Questions like, “Is the artwork properly stored for a long sales wait?” Like, “Is the artwork in the possession of Masterworks directly?” All of these questions could be easily resolved if Masterworks owns and operates a set of galleries… or at least a showroom at the bare minimum.

Additionally, with Masterworks ownership of galleries, this means you, as an investor, can physically go see the art you’ve invested in. You can see if it’s as it appears in the images. You can see it on exhibit, or at least it can be brought out for a viewing. You can see that it’s being kept and stored in appropriate environmental conditions.

There are so many questions surrounding the art itself, there is absolutely no way I would recommend anyone to invest in Masterworks… unless you absolutely like throwing money away on odd “investment” strategies. Knowing where that art is, how it’s being stored and if it’s being stored appropriately combined with knowing you’re able to view the actual art is extremely important BEFORE investing any money in a share of a painting.

Ponzi Scheme?

While I previously made reference to Bernie Madoff and his ponzi scheme, that statement isn’t intended to suggest that Masterworks runs a Ponzi scheme or that it intends to make off with your money. However, because of so many lingering questions, this business model seems unnecessarily risky… especially not knowing the answer to far too many questions surrounding the paintings.

Additionally, because of the volatility in art sales, as an investor, you must fully trust and be reliant on Masterworks buyers and appraisers to locate “valuable art” that might sell for some amount of money higher than what was paid. However, you’ve no idea if the art they’ve selected will actually sell at all. Because art is so subjective, what a few like, too many others may hate.

It also means betting that some nebulous “whale” will come along and snap up that piece of art (for millions) you just so happen to have invested in. That isn’t likely to happen often. Unless the art is of great historical value (i.e., Leonardo DaVinci or Michaelangelo or even more recent artists like Mark Rothko, Roy Lichtenstein or Marcel Duchamp), art produced by artists living and working today might fetch random amounts, but perhaps not millions. There’s just no way to know what any piece of art might fetch when produced by today’s artists. It’s all a calculated, but a seriously risky best guess.

Unfair to Artists

One thing Masterworks also seems to be attempting is to force art to be sold at far higher prices than it’s actually worth. This is what many collectors attempt to do, usually via auction. That is, Masterworks appears to intend to artificially inflate art prices to make better returns on shareholder investments. The difficulty is that this artificial inflation (nor does the sale itself) benefit the artist at all.

Where Masterworks might “buy” a work for $70,000 from an artist via a gallery, they may attempt to turn it for $1.3 million. That nets a huge profit for Masterworks and a lesser amount for shareholders in that work. However, for the artist, $70k is all they have received. The artist is not fairly compensated from a Masterworks sale.

One might argue that aftermarket sales of art never has benefited the artist. Yes, but here’s a business model that could arguably help bring artists into the fold by making sales on behalf of the artist. This goes hand-in-hand in owning galleries. Instead, it seems Masterworks has chosen an aftermarket sales model that excludes the artist. A model that only makes money for investors and Masterworks, but not for the artist. Intentionally leaving the artist out of this process is entirely greedy and unfair to the artist.

Artists Deserve Compensation

One might think that $70,000 is a lot of money for the sale of a painting. It is. But, it is nowhere near the amount that the artist could have netted if they had sold it for $1.3 million.

Artists shouldn’t be required to invest in their own paintings with Masterworks just to net more profit on an aftermarket sale. Instead, Masterworks should work directly with artists to list the work and then compensate the artist for at least 50% of the sale, either directly or by issuing a 50% ownership stake in the art via shares. The rest of the profits should go to paying out shareholders. This model would not only fairly compensate every artist, but it also fairly compensates the shareholders and Masterworks itself.

Artists are always the one who seem to get the shaft. This problem has existed for many, many years. Masterworks can modify their business model to make sales that directly benefit the artist while also properly compensating shareholders and turning a nice profit for Masterworks. Instead, it seems they have ignored this aspect only to make their sales benefit mostly Masterworks executives the most, leaving out the artist.

Artists vs Corporations

If you’re of the mindset that you would like to see artists fairly compensated for their work, skip these risky investment schemes and buy directly from an artist. If you buy directly from an artist, you are helping that artist, not some random corporate executives operating a more or less faceless and questionable company. If you’re willing to shell out $20 to see a movie actor perform, then why wouldn’t you be willing to pay an artist for the artwork they produce?

Not only can you carry pride in the fact that you purchased art directly from the artist, you also own an original work of art in full, not solely just a share in a work of art that you’ll never see. You can also hold pride in knowing that you have helped the artist produce even more work. Buying art from Masterworks does not, in any way, encourage artists to continue to their craft. In fact, the pittance that the artist might receive in the first sale may be barely enough to cover the time and effort put into producing that painting let alone help them produce future paintings. Art supplies are expensive.

Art Valuation and Secondary Market

Let’s talk about the investing and trading pieces. Masterworks operates a secondary market where shares can be traded. Unlike Wall Street stocks where a stock’s value is based on such fluctuating data points as company profits, company revenue, investor calls, product sales and announcements, analyst recommendations, investor confidence and volume of trading, paintings have no such intrinsic back end data points (other than perhaps trading volume… and even that is drummed up via this questionable investment scheme).

Art valuation is entirely subjective, made solely by a random person appraising its value. What that means is that if you invest in a work that claims to have a $30 “share price”, you’re at the mercy of an appraiser to raise or lower this price. Bid and ask sale prices might influence pricing some, but the pricing seen on the secondary market site is mostly “best guess”. There’s nothing behind that painting to “prop up” its changing value. There are no profit margins, no new product announcements, no analyst calls, no company books to review, nothing. It’s a painting. That’s it. Paintings don’t randomly change value UNLESS they are sold. Anything else purported is a dubious scheme.

Investing in a painting with a fluctuating value is a false equivalence to stock. There’s nothing there to change the value of the share in a painting, yet it seems that the values do change. Why? The painting hasn’t yet sold, so it makes zero sense. As I said, there’s nothing in any painting to justify changes in the share price until AFTER it’s sold. Once a painting has been sold, then the share price will change to reflect the sale price of the painting.

If Masterworks intends to see a painting’s share price fluctuate daily, like stocks, then there’s something seedy, dubious and awry going on. It’s also something that you as an investor need to understand before investing a cent. Intraday changes in painting’s share price prior to a sale is extremely dubious.

One might argue that there are a limited number of shares in the painting. That each share sold makes every share more valuable. I might be willing to accept that argument except a painting can be arbitrarily divided 100 times, 1,000 times or even 1 million times. When does that share division end? You can’t really divide a painting up like that. If you’re going to apply a random investment concept, such as a share, onto a painting, then any division into shares is entirely arbitrary and disconnected and holds effectively a fractional value tied to the current “worth” of the painting. Ultimately, there’s only one (1) painting. Therefore, there should only be one (1) share. When you buy that one (1) share, you buy the painting.

Having this sub-construct of many shares which are separate from the “painting as a single commodity” is not only an odd concept to apply to a physical object, it might be seen as a form of Ponzi scheme. These “shares” are actually an abstract idea applied to a single physical object which cannot be subdivided physically. So, how exactly does this abstract division concept work? That’s exactly what Masterworks is attempting to find out. It’s also why the Masterworks business model is unproven.

Overall

I can’t recommend investing “shares” in paintings via Masterworks for reasons already outlined above. However, let me summarize these points:

- Proper art storage isn’t explained (very high risk)

- Returns on investment isn’t fully explained (high risk)

- Paintings aren’t guaranteed to sell (high risk)

- No sales benefits given to the artist (problematic)

- No galleries to physically view or confirm ownership (exceedingly high risk)

- Art prices are highly volatile (high risk)

- Art sales are solely dependent on subjective criteria (overly risky)

- Art values are solely dependent on Masterworks “appraisers” (highly risky, requires high trust)

- Intraday changes in share prices are nonsensical prior to the painting being sold (dubious)

- Must trust Masterworks for both valuation and truth (overly risky)

- Must trust Masterworks that they actually own and possess the art (exceedingly risky)

- Secondary market attempts to treat shares in a painting like stocks (exceedingly risky & dubious)

Without seeing the painting physically, as an investor, you have no idea if Masterworks truly has that painting in their possession. It’s easy to take a picture and put it on a web site, making claims that they own and possess the work. This then tricks the investor into a purchase. Then, you hold and hold and hold and the painting never sells. In fact, you could come to find they don’t even own the original art. You might find that they’re selling something they don’t even have possession of.

While Masterworks may own some of the work they claim to own, there’s literally no way for an investor to confirm that every piece of art listed is actually in the possession of Masterworks. This problem is exacerbated mainly because Masterworks operate no galleries.

For this reason, Masterworks could be selling you shares in a work that they do not, in fact, own or possess. That’s effectively a form of fraud.

Masterworks would do best to modify their business model to offer a process that can prove they physically own the paintings they claim to own. The only way this is really possible is if they open and operate at least one Masterworks gallery somewhere so shareholders can visit and request a viewing of the art they’ve invested in. This is effectively an audit system which holds Masterworks accountable to all shareholders. Without this change in their business model, investing in any work that Masterwork claims to own is unnecessarily risky. To anyone willing to give money to this company, I say, “caveat emptor!” Let the buyer beware.

Without such basic investor auditing responsibilities, I strongly recommend staying away from this novel, but highly problematic investing concept and stay away from Masterworks as a corporation. That’s not to say this concept can’t be revised to be more functional, but at the moment this concept is just not there. This concept forces an over-burdensome amount of trust and risk onto the investor and off of Masterworks, while leaving too many unregulated, unauditable and manipulable pieces in the hands of Masterworks executives.

Bottom Line: If an employee at Masterworks wished to game the Masterworks system, the lack of proper auditing over this concept would allow any executive far too easy access to game it… thus losing investments from investors and truly turning this into a huge fraud scheme.

Business Concept: B

Business Execution: F+

Scam Risk Level: Exceedingly High, Stay Away

Recommendation: Don’t Invest in Masterworks

↩︎

COVID-19: Fact vs Fiction

Detective work is an art, not a science. However, Dr. Sanjay Gupta attempts to be all things to all people, yet fails at being a journalist or a detective. He definitely shouldn’t quit his medical day job, that’s for sure. Let’s explore.

Fact vs Fiction

Sanjay Gupta hosts a CNN podcast that purports to separate fact from fiction when it comes to matters all things medical. However, in his CNN podcast on February 24th, 2021, this podcast does everything except separate fact from fiction.

On this episode, Sanjay Gupta speaks to random person Peter Daszak, a rando with a British accent (which Sanjay seems think lends his words some credibility) who purports to be some level of official on a mission for the World Health Organization. We’ll circle back around to Peter Daszak’s involvement in this shortly. This person claims to have visited Wuhan and then spouts all sorts of rhetoric as to the origins of COVID-19. As this podcast progresses, this guest digs an ever deeper and deeper hole about the wet market origins with Sanjay capping it with question similar to, “Does this rule out COVID-19 having begun in a lab” (paraphrased).

I’m getting ahead of myself a little. Daszak makes a bunch of statements about the wet market as having been the possible origin, but then always qualifying his statements as “coulda”, “woulda” and “shoulda”. For example, he claims that the markets had a lot of frozen meat. I’m sure it did. Yet, none of that meat tested positive. In fact, in every case where he mentions a type of meat, none of it tested positive for COVID-19. Then he later mentions other additional wet markets where some people might have visited as a possible origin. Yet, no mention of testing or of any positive outcomes from those wet markets. Deflection at its finest. Let’s continue, shall we?

“See only what you want to see”

This is where fiction trumps fact. In fact, it seems as this podcast progresses, Sanjay and Daszak both heavily wish to see the wet market as the origin, yet even having over 900 samples from the original Wuhan wet market with none testing positive for COVID-19, that logically and clearly says that the wet market wasn’t the origin. If you want to believe science here, the science of zero COVID-19 samples in any of the food tells us that the wet market was definitively not the origin… at least, not by food.

Because people tend to congregate in markets en-masse to buy their groceries, it may have been an origin only because of a human-to-human transmission super-spreader event.

Of course, both Sanjay and Daszak espouse “follow the science”, yet there is no science at all involved in direct detective work. Science may be utilized as a tool in detective work, but using science as a detective tool has failed to uncover the wet market as a food origin. If any wet market in China had been an origin for COVID-19, at least some food samples should show positive somewhere. Yet, they don’t.

Sanjay and Daszak seem to be in this podcast to sway minds through disinformation, not actual information. Actual information shows proof. Daszak clearly has none, but then there’s subtext for his motives (more on that below). That lack of proof means that this podcast is attempting to spread disinformation by pointing fingers towards the wet market and away from the Wuhan Institute of Virology.

China’s Agenda

China wants to be let off of the hook for the spread of COVID-19. They want this so badly that they’re willing to do or say anything to make that a reality. China doesn’t care about lying or disinformation. In fact, they’re more than happy and willing to see credible “western” medical scientists put their reputations on the line to tow China’s “we’re innocent” line. China is not innocent in the spread of COVID-19, but then neither are other countries.

It’s unmistakable. COVID-19 began in Wuhan, China. It didn’t begin in Singapore or Italy or South America or anywhere else in the world. It began in Wuhan, China. It’s also clear that we have no proof that it began in wet market food… which means that it likely began via human-to-human transmission… which means there is a patient zero.

Patient Zero

Where is patient zero? As a professional medical scientist, THIS is the question Dr. Gupta should be asking. Instead, he’s asking questions about the wet market in an attempt to pin this firmly on animal to human transmission via food. Yet, when all of the samples from that wet market are scientifically tested, nothing confirms that the virus began at the market… or at least it didn’t begin via consumption of a tainted animal purchased at the market. If COVID-19 began in a wet market, it began because of a human super-spreader event.

We already know exactly how transmissible this virus is. We also know that it can live on surfaces, sometimes for days. This means that COVID-19 could easily have begun by patient zero visiting a wet market… which is a common practice for buying food in China.

Again, where is patient zero? We already know the Wuhan Institute of Virology had both been studying and housing animals infected with a variant of SARS-CoV-2 (aka COVID-19). The lab workers had been tending to the animals, including cleanup of their feces and urine. There is some question as to whether the WIV’s safety procedures had been properly followed prior to the release of COVID-19 in early December 2019.

On the one hand, you have a wet market of animals, none of which have tested positive for COVID-19. On the other, you have the Wuhan Institute of Virology which houses animals known to test positive for COVID-19. I’ll let you do the math here.

While Sanjay and Daszak are adamant that it “must” have started in the wet market, Ocham’s Razor disagrees. The simplest answer is that COVID-19 got out of the lab. Let’s understand how.

Lab Release?

Around the time that COVID-19 (or at least an unknown illness) began to show in China in early December, a lab assistant went missing from the Wuhan Institute of Virology. Her name was Huang Yanling. The lab director, Shi Zhengli, has continually disavowed that the virus escaped from her lab. Yet, this missing lab assistant has never been accounted for. It has been assumed that Ms. Yanling was actually patient zero. Through that supposition, she may have been the person who first became infected, spread it around Wuhan in a super-spreader event and then may have died from it… with her body having been burned.

Ocham’s Razor asks, “Why?” Because she (along with others in the lab) worked at the Wuhan Institute of Virology tending to the infected animals. But then, she vanishes without a trace? Is she alive or dead? No one seems to know and Shi Zhengli shrugs this disappearance off as normal.

When you’re dealing with an outbreak like COVID-19, you can’t discount missing lab assistants from the equation. Yet, Dr. Sanjay Gupta and Dr. Anthony Fauci seem to ignore this logic and conclusion jump right over to the diversion of the wet market… which, again, has effectively been proven not to have been the cause of the outbreak.

Again, on the one hand, we have no proof that any wet market animal has tested positive (science). On the other hand, we have a missing lab assistant from the Wuhan Institute of Virology with no explanation of their whereabouts (detective work). Sure, it seems circumstantial, but no one has done an official investigation. Not the WHO, not the CDC, not China and not the United States.

Like a magician who wants your eyes staring at his right hand while his left does the switcharoo so you don’t see how the trick is done, the WHO, China, the U.S. and the worldwide medical community want you looking at the wet market while a young lab assistant, Huang Yanling, disappears from a lab housing COVID-19 infected bats. Yeah, if that’s not misdirection at its finest, I don’t know what is.

Bats and COVID-19

It’s widely agreed that COVID-19 began in bats. Which animals were housed at the Wuhan Institute of Virology? SARS-CoV-2 infected bats, of course. Captive animals don’t just clean up their feces and urine on their own. People must clean it for them. To do this, lab assistants must wear the proper hazard protection gear to avoid accidental exposure while cleaning up the animal waste. Without proper protections, transmission from animal to human can become a reality. Did the WIV fail to properly set up hazard protection? Did this lab assistant fail to wear said protective gear at all times? This lab had already been warned of improper safety procedures years before the incident.

Two State Department cables show that American embassy officials in Beijing made several visits to the research facility and sent two official warnings back to Washington in early 2018 about the lab’s inadequate safety measures. This was at a time when researchers were conducting risky studies on coronaviruses from bats, The Washington Post reported, citing intelligence sources.

https://www.voanews.com/covid-19-pandemic/chinese-lab-checkered-safety-record-draws-scrutiny-over-covid-19

Let me put it this way… which is more likely?

- Someone ate an infected bat from a wet market? or..

- A lab assistant not following established procedures released COVID-19 from the lab via themselves?

Considering that this lab had been warned of improper safety procedures in the past, I’ll let you do the math. It’s not hard math either. Again:

- Are we looking at infection from a wet market, which hasn’t found a food sample with COVID-19?

- Are we looking at infection from a lab with known unsatisfactory safety procedures and a missing lab assistant?

Occam’s Razor is fairly clear here. So is K.I.S.S. (keep it simple stupid). Logic dictates that it’s #2 as the source, not #1. Regardless of what people have stated, it’s fairly clear that the Wuhan Institute of Virology is the most likely candidate. The question, why aren’t more news outlets, the government and other officials like Dr. Fauci and Sanjay Gupta looking in this direction?

Conflict of Interest

Most doctors look up to Dr. Fauci as their guide for all things COVID-19. Unfortunately, Dr. Fauci isn’t as innocent in all of this as he appears. Dr. Fauci headed up the NIH at a time when that organization helped fund the Wuhan Institute of Virology to the tune of over $700,000, perhaps more. This funding was for Gain of Function research.

It gets worse.

“Oh, what a tangled web we weave.”

Who exactly is Peter Daszak? I’m happy you asked that. He runs EcoHealth Alliance, a British non-profit that, in 2018, identified the possibility of SARS-CoV-2 variants, over a year before the pandemic. Why were they able to do this? Because this British non-profit funded research through the Wuhan Institute of Virology. Where did EcoHealth Alliance get its money? From the United States government, of course. Remember that over $700,000 above? Yeah, that’s where some or all of it went.

That money was funneled from the United States NIH to EcoHealth Alliance and then apparently that money landed at the Wuhan Institute of Virology for virus research. It’s not like EcoHealth Alliance is a direct research firm. Nevermind that the Obama administration had banned the use of funds to further Gain of Function research related to viruses in 2014 to prevent this situation from unfolding. Unfortunately, that ban was lifted in 2017 by the NIH (headed by Fauci), leading to further research and perhaps directly to this pandemic. Without that money funneling through outfits like EcoHealth Alliance to such subcontractors as the Wuhan Institute of Virology, the world might not be in this situation.

It takes money to operate expensive research facilities. Without that money, no facilities. Of course, the U.S. Government doesn’t want to get involved in such risky research directly or have that research on U.S. soil, which could backfire on the United States. Instead, it’s fine to funnel money through intermediates so that the United States can absolve itself of involvement through plausible deniability… even though it’s as plainly obvious as it is here. The U.S. indirectly funded research that lead directly to the COVID-19 outbreak.

Is China still at fault? Most certainly. That facility is located in China. China operates it. It is completely on China to operate such facilities responsibly and safely. However, the United States NIH cannot disavow involvement when a very large sum of money landed at that lab, helping them fund SARS-CoV-2 research and possibly leading to the virus’s release. It’s particularly worrying when considering that this research lab indirectly received funding from the NIH, headed up by Dr. Fauci at the time. Dr. Fauci had to know where that money could or would end up. Even still, the NIH could have asked how that money was to be spent by its recipients.

Plausible Deniability and Gupta’s Podcast

I have no idea how culpable or complicit Sanjay Gupta may be in this situation, but it is entirely irresponsible to host a person like Daszak by allowing them to push the wet market disinformation as the source when there has been no actual science proving the wet market’s direct food involvement.

Instead, Daszak’s culpability and possible complicity is evident by his non-profit’s funneling of money into the Wuhan Institute of Virology, which firmly places him, EcoHealth Alliance and its reputation at risk. No. He can’t risk that. So, going on a show like Dr. Sanjay Gupta lends credibility to his assertions that the wet market was the location where it began, never mind that science shows there’s no food evidence. However, a super-spreader event is definitely not out of the question. But then, the question arises, who was patient zero and where began their super-spreader event? I think we already have the answer to that question above.

For this reason, it’s important to read articles and understand the situation for yourself. Don’t take statements from people even who appear well intentioned at face value. You must dig deeper for answers to your questions.

We definitely haven’t gotten the whole answer from China or from the United States. Instead, the media, medical professionals like Dr. Sanjay Gupta and Dr. Anthony Fauci have danced around the issue. With this article, it’s clear to see why they are doing so. To put forth any other narrative about where and how the virus began puts their own careers in jeopardy.

Unfortunately, mainstream media would never pick up such an article like this because it damns not only such people like Dr. Fauci, it damns their own journalistic credibility because the United States government won’t play nice with them after such an article, citing them as “wild conspiracy theorists”.

Being labeled a “conspiracy theorist” is much the same as being accused of sexual misconduct these days. It’s enough to get you fired and labeled as a “nut job”. When, in fact, there’s nothing at all nutty about the statements. In fact, it’s just the opposite. However, even if Dr. Fauci is a “nut job”, he’ll never be openly called that because of his position within the United States government.

For this reason, it’s why we are now facing a political rift across party lines. It’s why Republicans can storm Capitol Hill and most will likely be let off for “good behavior”. Can’t have “well meaning” Republicans being held to justice for damaging property and killing people. Since when is a playing a party affiliation card now a “get out of jail free” card? It seems this, along with the above, is the state of affairs these days.

Dr. Sanjay Gupta needs to rename his podcast. It’s not about Fact or Fiction, it’s about perpetuating disinformation and lies. With Trump, we’ve already had enough lies to last a lifetime. We don’t need yet more lies being spouted from supposed medical professionals. This is why you must question everything.

Update for June 2, 2021

As of June 1, 2021, many of Dr. Fauci’s early pandemic emails from 2020 have been released based on a Freedom of Information Act (FOIA) request. From these emails, there’s much to read. Too much to really discuss here. With the release of these emails, suffice it to say that Fauci’s world is beginning to unravel. FOIA is one of those bane freedoms that people who work in the government would like to see abolished. Thankfully it exists and eventually allows unclassified government documents to be released to the public. I’d suggest reading the emails for yourself. However, as of this update, I’m at a loss to find a site that archives only the text of these emails. For now, you’ll need to visit news sites.

Searching Google for only the emails leads to what I deem ‘spearch‘, a combination of the two words spam and search. It’s when a site like Google chooses to bring garbage listings to the top of the search results rather than the search results you’re actually wanting. Google’s search panel’s AI understands exactly what you want, but instead, it intentionally usurps those results by planting garbage results, which attempts to direct you to those garbage sites with useless information for the sake of more ad revenue.

If I can find a site that simply allows reading only the email test without all of the unnecessary and extraneous garbage content, I will update this article.

↩︎

How does Twitter Philanthropy work?

How does all of this Twitter philanthropy actually work? Let’s explore the seedier side of it.

Twitter Philanthropy Exposed

I won’t name any specific accounts simply because there are too many of these accounts preying on people’s needs, but let me expose how these accounts REALLY work. There is one on top of this pile, but I will let you find it yourself. If you search Google for the key words “Twitter Philanthropy“, you will find this specific Twitter account within the first 10 search results. But, don’t go run over there just yet to follow it before reading this article.

Twitter Impersonation

Let’s start this out by explaining how these accounts operate. While some of these large Twitter philanthropy accounts purport to be operated by a single individual, they are not. Instead, they are operated by a team of individuals who have access to this single Twitter account so named for a single person. In fact, this situation is in violation of Twitter’s Terms of Service rules of impersonation.

Impersonation is a violation of the Twitter Rules. Twitter accounts that pose as another person, brand, or organization in a confusing or deceptive manner may be permanently suspended under Twitter’s impersonation policy.

By operating an account as a team, rather than by the single individual named on the account, this is definitely impersonation… regardless of whether the single individual has authorized that “team” for that purpose.

If you are interacting with a Twitter account who appears to be a single person, but unbeknownst to you there are actually multiple people who are not the named individual operating that account, this is entirely deceptive and misleading… and the very definition of impersonation. You are not dealing with the person you think you are. This is in violation of Twitter’s rules. Whether Twitter sees it that way is entirely subjective and based on Twitter’s whims, unfortunately.

Team Accounts

There are many team operated accounts on Twitter. Many celebrities operate such accounts. Since the celeb can’t be at the account 24/7 to answer responses, they hire staff to manage these tweets. Most times, these celebrities are represented fairly and appropriately by their hired staff, mostly because the staffers remain in close contact with the celebrity to make sure the tweets are appropriate to the celebrity’s brand.

With these philanthropy accounts, it seems these are much more loosely operated. The team is made up of people around Twitter who manage this account and have Twitter accounts of their own. They don’t always seem to have direct approval of the account owner. If you read through some of these philanthropic account tweets, they seem to show random and incoherent tweet-to-tweet messaging, espousing differing and hypocritical ideals. Why? Because different people are posting these tweets to that single account under the guise of impersonating a single person.

Philanthropy Exposed

While these accounts may have started out as genuine philanthropy, they have degraded into an odd scam that takes advantage of people’s needs… and mostly exist as ways of gaining followers. Worse, these accounts breed even more scam artists. Scam artists who WILL take advantage of you and scam you in the process. I’ll talk about the scammers at the end and how those work. Let’s focus on the actual purported philanthropy accounts first.

Why a team?

Good question and one that you’ll understand once I explain it. Basically, when more team staffers are attempting to locate money from other contributors, that means more money to share in the guise of philanthropy under that single Twitter account. Looking for contributions isn’t the problem here, though. It’s the scammy WAY that this team goes about looking for contribution money. If this single aspect doesn’t leave a bad taste in your mouth, keep following along as it gets so much worse.

The team that makes up the single top Twitter philanthropy account uses Twitter (and sites like GoFundMe) to gain money first. Instead of actually giving out money from the purported account owner, the team actually solicits money contributions from random people using dubious methods including begging, groveling and outright scamming using sites like GoFundMe. These team members are then adding their ill-gotten money into that Twitter account’s philanthropy fund for giveaways.

Here’s where the deceptive part comes in. This team of people collect these monies using their own personal accounts, accounts not associated with that Twitter philanthropy account. This makes it difficult to trace where that philanthropy money actually came from. Deceptive and a form of money laundering. Dirty. When other people contribute their money to one of these outside accounts for some possibly even fake purported need, this is a huge problem for these larger philanthropist accounts. Any money given out by a philanthropist shouldn’t have been obtained by using a scam. Yet, here we are.

Yes, this means this team is not actually giving out the philanthropy account owner’s money, as is implied by the account owner’s statements. Instead, that team is raising funds using outside means, possibly using deceptive means (claiming to be raising money on behalf of a veteran or claiming to have a high electric bill). Then, they take that money that has been raised and give it out on Twitter. Do they give out 100% of that contributed money? Do they use the money towards the claimed need? My guess to both of these questions is no. These philanthropy accounts might be keeping as much as 50% or more of the money they collect and, in turn, only give out 50% or less of those ill-gotten contributed funds.

It’s one thing to solicit money for an intended purpose and use it for that purpose. It’s entirely another to solicit money for a purpose, not use it for that purpose and give it away to someone on Twitter. Full disclosure here? Yeah, no. Not to mention the tax ramifications of such a setup.

Giving Money Away

While giving away money might seem a good thing, this action actually preys on people in need. Worse, the way these accounts are being managed is dubious at best. Yes, it gets even worse. These accounts have so many followers that they can’t possibly manage what gets written into their Tweets. What you’ll find in most of the Tweet replies consist of people claiming to also give away money. I’d bet that at least 99.9% of these people dropping in Tweet replies are scammers looking to part you from your money. It might even be some of the team running that same philanthropy account looking for money for their next “giveaway”.

This is why this situation is a double whammy for those in need. Not only is there so little money given away from these top Twitter philanthropy accounts (they can only raise a couple hundred dollars at a time usually), the Tweet replies are chock full of scam artists willing to take advantage of you.

The act of giving away this money on Twitter might seem altruistic, but I guarantee you that it is not. There is no altruism going on here. It’s all about gaining followers on Twitter and making it SEEM like the account is altruistic. It’s just a show. The reality is, it’s a business that follows the following formula:

- Team hides behind Philanthropy account (unbeknownst to Twitter followers)

- Team is tasked to raise money (using whatever dubious means necessary) from random individuals, each team member raising money separately using their own individual accounts

- Team places raised money into Twitter account fund for “giveaways”

- Team likely keeps much of that money for themselves as “payment”

- Twitter Philanthropy occasionally awards random folks for random reasons

What if I win?

If you are one of the very few who manage to get picked to receive money from a philanthropic Twitter account, don’t think it’s all roses. To receive any money, you are required to jump through legal hoops before that money is deposited into your account.

“What legal hoops?”, you ask. Good question. You are required to agree to a long, stringent set of terms and conditions before you are awarded any money. These conditions allow this Twitter philanthropy account to do whatever they want with your win while restricting you. What document would I sign? You will need to read and sign a Non-Disclosure Agreement (NDA) and return it to the team operating the philanthropic account before you can take possession of that $20 or whatever small amount they are willing to give you. This is the very definition of victimizing someone in need. Someone in desperate need of money would be willing to sign just about ANYTHING to get that “free” money.

Once you agree to their restrictive terms and conditions, they will send you that money via CashApp or whatever other agreed upon payment system. If you violate these terms, they will sue you.

This is not a no-strings-attached way to get money. In fact, it wouldn’t surprise me to find that some of these “charity acts” might actually be loans which must be repaid at some point in the future. In other words, be very, very careful if you choose to attempt to get money out of these philanthropic accounts. They may screw you on the way in and on the way out… and perhaps even later in the future.

Twitter’s Response

Unfortunately, Twitter (the company) doesn’t monitor or manage any of these philanthropy accounts. They allow them to operate with impunity. Because it seems that these philanthropic accounts “appear” (it’s all about appearances) to be doing good for the community, Twitter (the company run by Jack Dorsey) turns a blind eye and allows this bad situation to continue and fester. Few people actually get anything good out of these accounts. Even more are getting scammed from the tweet replies claiming to also give away money for following and retweeting. Don’t fall for any tweet replies. They’re almost certainly a scam.

Essentially, Twitter is turning a blind eye to these accounts which, in fact, do not perform a “good service” for Twitter. In fact, there are likely more people being scammed out of their money than ever receive money from any Twitter philanthropy. On Twitter, it’s not okay to write about certain controversial topics, but it’s perfectly acceptable to take advantage of people in need and scam them out of even more money? Thanks for looking out for us, Jack!

Scams and Philanthropy

As I stated earlier about Tweet replies in the article, let’s now understand how you can get scammed through fake philanthropy on Twitter. There’s actually more fake philanthropy going on Twitter than there is genuine philanthropy.

In fact, it’s very easy to get scammed out of money on Twitter. This specific scam isn’t what the top philanthropy accounts are using, however. Instead, they use the model described above, which is nearly as seedy. With that, let’s look at how fake philanthropy accounts on Twitter attempt to part you from your money so they can sip champagne on a beach.

This next philanthropy scam is bait and switch and it’s the primary way they scam you. How this one works is that you’ll see someone Tweet replying they’re willing to give you money and all they need is your CashApp tag sent to them over a direct message (DM). You then give it to them. Seems harmless enough, right?

The Scam Begins

Over the DM area, they’ll start by asking you a lot of seemingly personal questions. If you pass all of these probing questions, they’ll explain to you that their CashApp app is broken and that they can’t use it. They’ll tell you they need to switch to using PayPal. Here’s where the scam actually begins. Any philanthropy person who switches the payment method sets up a HUGE RED 🚩. Don’t fall for this. If the person can’t use CashApp, which enticed you in, to send you the money, walk away. CashApp can be used by anyone and it can be set up quickly. Any excuse someone gives for not using CashApp is fake.

When they switch to using PayPal, they can then claim to need you to send them money to cover fees or other such nonsense to complete the PayPal cash transfer. In that goal, they’ll issue you an invoice to pay. This is the scam. First, PayPal doesn’t need money to complete a cash transfer. Anyone making this claim is scamming you. Second, you shouldn’t need to pay any money to get money. If they can legitimately pay you, they will pay you no strings attached. Third, remember that they roped you in by offering the use of CashApp, then inexplicably switched to PayPal (bait and switch).

Anyone who can legitimately pay you money can do so using CashApp. There is no need to switch to another service. You can read more about PayPal scams here, and there are plenty more just like this one.

Screenshots

To attempt to trick you further by making themselves seem legit, they will send over a screenshot showing that they paid someone else money. A screen shot is EASILY faked, let alone found on the Internet. There’s no way to verify that any screenshot they send you is in any way linked to them (or even legitimate). In other words, screenshots are not proof of anything, let alone of being charitable.

If the person is legitimate, they will send you the money without asking you for anything in return. If they ask for anything in return, it’s a scam.

Uncomfortable Questions

Other behaviors they might exhibit is asking a series of deep probing questions you might not feel comfortable answering. Specifically, question like what bank you are using, what credit card companies you have, and so on. That’s none of their business. If they’re willing to send you money under philanthropy, they don’t need any of this information. If they begin asking probing questions like social security numbers, birth dates, actual account numbers or any other deep personal information, this has the hallmark of scam all over it. Remind them that the CashApp tag is all they need to send over money. If they can’t do this simple one thing, then they’re not legitimate.

Philanthropy should be about the good in giving, not finding out as many personal details about a person as possible. If someone begins asking very deep diving personal questions about you, your location and your finances, walk away. Explain to them that they don’t need that information to be charitable. If their charity relies on this information, they can find someone else.

Chances are, the reason they are asking these personal questions is to not only scam you, but take the rest of your accounts for a ride.

The Dark Side of Twitter Philanthropy

Yes, there is actually an extremely dark side to Twitter philanthropy which has now been exposed showing just how dark it can get. No, Twitter philanthropy is not all roses, as some adamantly claim.

For a moment, let’s suppose you do win the philanthropy lottery. Let me ask you this simple question. As a recipient of that supposed good will money, do you really want to accept that money not really knowing if someone behind that philanthropy account scammed another to give you that money?

Yeah, I wouldn’t want to either. Money can be helpful, but not at the cost of someone else being scammed out of it. Be careful and tread lightly when following any Twitter philanthropy accounts. Keep your guard up and watch out for people on Twitter claiming to be altrustic do-gooders. In these especially hard times, don’t fall for fake altruism. If you are really in need of money, head over to GoFundMe and plead your own case with your money raising efforts. The money you raise at GoFundMe will be yours without such underlying strings. If you’re putting your hand out towards someone else’s wallet, particularly on Twitter, expect the worst in people.

In fact, let me point you to this exposé article describing one particular philanthropy account on Twitter. This article is a bit disjointed of a read, but if you can follow it, you will better understand this very dark and seedy side of Twitter Philanthropy in excruciating detail.

↩︎

What’s wrong with Quora?

![]() You might be asking, “What is Quora?” We’ll get into that soon enough. Let’s explore the problems with Quora.

You might be asking, “What is Quora?” We’ll get into that soon enough. Let’s explore the problems with Quora.

Questions and Answers

Before we get into Quora, let’s start by talking about Google. Many people seek answers from Google for many different questions. In fact, questions are the number one use for Google. You don’t go to Google to seek answers you already know. You go there to search (or question) things you don’t know. Such questions might include:

- Where can I buy a toaster?

- How long do I bake a chicken?

- How do I make Quesadillas?

- What’s the value of my 1974 Pontiac T-Bird?

These are full text questions. And yes, Google does support asking questions in long form such as these above. You can also search Google by using short key words, such as “toastmaster toaster” or “pontiac t-bird” (no, you don’t even need to use the proper case).

These short form questions are solely for use at search engines. When seeking answers to long form questions both Google and other sites can offer responses to your questions. One such site is Quora. Another is Yahoo Answers (a much older platform). Even Google got in on this action with Google Questions and Answers.

Quora

Quora is a recent incarnation of the older Yahoo Answers platform. Even before Yahoo Answers, there was Ask Jeeves. Even Epinions, a product review site (defunct as of 2018), had many answers to many questions. Epinions, in fact, opens a bigger discussion around site closures and content… but that’s a discussion for another article.

The real question (ahem) is whether sites like Yahoo Answers and Quora provide valuable answers or whether they simply usurp Google’s ability to answer questions in more trusted ways. I’m on the fence as to this question’s answer. Let me explain more about Quora to understand why I feel this way.

Quora is a crowdsourced product. By that I mean that both questions and answers are driven by crowds of subscribers. Not by Quora staff or, indeed, Quora at all. Unlike Wikipedia which has many volunteers who constantly proof, correct and improve articles to make Wikipedia a trustworthy information source, Quora offers nothing but the weakest of moderation. In fact, the only moderation Quora offers is both removal of answers and banning of accounts.

Quora has no live people out there reviewing questions and answers for either grammar and mechanics, nor trustworthiness. No one questions whether an answer is valid, useful or indeed even correct. Quora doesn’t even require its answer authors to cite sources or in any way validate what they have written. In fact, Quora’s moderation system is so broken that when answer authors do cite sources, their answer might be flagged and removed as ‘spam’. Yes, the very inclusion of web site links can and will cause answers to be marked as spam and removed from the site. Quora’s insane rationale is that if there’s a web link, it must be pointing to a site owned by the answer author and in which the answer author is attempting to advertise. This stupid and undermining rationale is applied by bots who neither read the content they review nor do they understand that the answer author can’t possibly own Wikipedia.com, Amazon.com or eBay.com.

Indeed, Quora’s moderation is so bare bones basic and broken, it undermines Quora’s own trustworthiness so much so that when you read an answer on Quora, you must always question the answer author’s reputation. Even then, because Quora’s verification and reputation system is non-existent, you can never know if the person is who they say they are. But, this is just the tip of the troubles at Quora.

Quora’s Real Problems

Trustworthiness is something every information site must address. It must address it in concrete and useful ways, ways that subscribers can easily get really fast. Wikipedia has addressed its trust issues by a fleet of moderators who constantly comb Wikipedia and who question every article and every statement in each article. Even with a fleet of moderators, incorrect information can creep in. Within a day or two, that information will either be corrected or removed. Wikipedia has very stringent rules around the addition and verification of information.

Twitter (prior to Musk having bought it) offered a verification system so that celebrities and people of note could send information to Twitter to verify who they say they are to Twitter’s staff. You’ll notice these as little blue check mark’s by the Twitter subscriber’s name. These check marks validate the person as legitimate and not a fake. HOWEVER … After Musk’s takeover of Twitter => X, the blue check has become nothing more than a useless symbol that someone paid a few bucks to X. The former trust that the blue check mark offered prior to Musk became entirely worthless after anyone could buy it with no verification.

Quora, on the other hand, has no such rules or validation systems at all. In fact, Quora’s terms of service are all primarily designed around “behaving nicely” with no rules around validation of content or of authors. Indeed, Quora offers no terms that address trust or truth of the information provided. Far too many times, authors use Quora as a way of writing fanciful fiction. Worse, Quora does nothing to address this problem. They’re too worried about “spam” links than about whether an answer to a question is valid or trustworthy.

Yet, Quora continually usurps Google’s search by placing its questions (and answers implicitly) at the top of the search results. I question the value in Quora for this. It’s fine if Quora’s answers appear in search towards the bottom of the page, but they should NEVER appear at the number 1 position. This is primarily a Google problem. That Google chooses to promote untrustworthy sites at the top of its search results is something that Google most definitely needs to address. Sure, it is a problem for Quora, but it’s likewise a problem for Google.

Google purports to want to maintain “safety” and “trustworthiness” in its search by not leading you to malicious sites and by, instead, leading you to trustworthy sites. Yet, it plops Quora’s sometimes malicious answers at the top of its search results. Google needs to begin rating sites for trustworthiness and it should then push search results to appropriate levels based on that level of trust. Google needs to insist that sites like Quora, which provide consumers with actionable information, must maintain a certain level of trust to maintain high search rankings. Quora having its question results appear in the top 3 positions of the first page of Google search based entirely on weak trustworthiness is completely problematic.

Wikipedia strives to make its site trustworthy… that what you read is, indeed, valuable, valid and truthful information. Quora, on the other hand, makes absolutely no effort to ensure its answers are valid, trustworthy or, indeed, even truthful. You could ask Google for the answer to a question. You might see Quora’s results at the top of Google’s results and click it. Google placing such sites in the top 3 positions implies an automatic level of trust. That the sites that appear in the first 3 results are there because they ARE trustworthy. This implicit trust is entirely misplaced. Google doesn’t, in fact, place sites in the top of its search because they are trustworthy. It places them there because of “popularity”.

You simply can’t jump to this “trustworthiness” conclusion when viewing Google search results. The only thing you can glean from a site appearing in Google results is that it is not going to infect your computer with a virus. Otherwise, Google places any site at the top of its ranking when Google decides to rank in that position. As I said, you should never read any implicit level of trust into sites which appear in the first 3 positions of Google search. Quora proves this out. Quora’s entire lack of trustworthiness of information means that Google is not, in any way, looking out for your best interests. They are looking out for Quora, not you. Quora’s questions sometimes even rank higher than Wikipedia.

Google and AI results

This section has been added in 2025 with new information regarding changes with Google Search. Google formerly relied heavily on Quora for questions and answers, because Google’s own answer site didn’t stack up. With the recent introduction of AI answers at the top of Google’s search results, Google has now pushed Quora out as a useful answer for most searches. Much of what was stated involving Google and Quora within this article has now substantially changed for Quora. No longer are Quora answers being promoted to the top of Google’s search. That spot has been replaced by Google’s AI answers system. That Quora has gotten bumped out of Google is a good thing. Unfortunately, what replaced it isn’t a good thing, at least not yet.

So, be careful. Google’s AI answers are likely to be even more untrustworthy and incorrect than Quora’s answers. Google’s AI answers are speculated to offer wrong information as much as 60% of the time.

Recent studies and user experiences indicate that Google’s AI Overviews can be wrong quite frequently. A study by the Columbia Journalism Review found that AI search tools, including Google’s, provided incorrect answers to over 60% of queries. Google acknowledges these errors and has even admitted to past mistakes, particularly in the early stages of AI Overviews. While Google is working to improve its AI, users should be aware of the potential for inaccuracies, especially with uncommon or complex queries.

Be cautious when relying on Google’s AI answers, but also be just as cautious when reading Quora’s answers. However, because Quora’s answers are more likely to be handwritten by human authors, those answers may end up correct more often than 60% of the time. Though, answer authors can now use AI systems like ChatGPT to craft their answers for Quora. Again, remain cautious. Now back to the regularly scheduled original article.

Quora’s Answers

With that said, let’s delve deeper into the problem with Quora’s answers. If you’ve ever written an answer on Quora, then you’ll fully understand what I’m about to say. Quora’s terms of service are, in fact, counter to producing trustworthy answers. Unlike news sites like CNN, The Washington Post and the L.A. Times, where journalistic integrity is the key driving force, Quora ensures none of this. Sure, Quora’s answer editor tool does offer the ability to insert quotes and references, but doing so can easily mark your answer as ‘spam’.

In fact, I’ve had 2 or 3 year old Quora answers marked as ‘spam’ and removed from view because of the inclusion of a link to an external and reputable web site. Quora cites violation of terms for this when, in fact, no such violation exists. The author is then required to spend time appealing this “decision”.

Instead, its bots will remove reviews from its site based entirely upon reports by users. If a user doesn’t like the answer, they can report the answer and a Quora review bot will then take the answer down and place it under moderation appeal. There is no manual review by actual Quora staff to check the bot’s work. This work is all done by robots. Robots that can be gamed and sabotaged by irate, irrational, upset users who have a vendetta against other Quorans.

The answer takedowns are never in the interest of trust or making Quora more trustworthy, but are always in the interest of siding with the reporting user who has a vendetta or is simply insane. Users have even learned that they can game Quora’s robots to have answers removed without valid reasons or, indeed, no reasons at all. There’s no check and balance with the moderation robots or takedown requests. Quora receives a report, the answer is summarily removed.

Unfortunately, this is the tip of a much larger Quora iceberg. Let’s continue.

Which is more important, the question or the answer?

All of the above leads to an even bigger problem. Instead of Quora spending its development time attempting to shore up its level of site trust, it instead spends its time creating questionable programs like the Partner Program. A program that, in one idea, sums up everything wrong with Quora.

What is the Partner Program? I’ll get to that in a moment. What the Partner Program ultimately is to Quora is an albatross. Or, more specifically, it will likely become Quora’s downfall. This program solidifies everything I’ve said above and, simultaneously, illustrates Quora’s lack of understanding of its very own platform. Quora doesn’t “get” why a question and answer platform is important.

Which is more important to Quora? They answered this question (ha, see what I did there?) by making the question more important than the answer.

That’s right. The Partner Program rewards people monetarily who ask questions, NOT by rewarding the people who spend the lion’s share of their time writing thoughtful, truthful, trustworthy answers. In effect, Quora has told answer authors that their answers don’t matter. You can write a two sentence answer and it would make no difference. Yes, let’s reward the people who spend 5 minutes writing a 5-10 word sentence… not the people who spend an hour or two crafting trustworthy answers. And this is Quora’s problem in a nutshell.

Worse, it’s not the questions that draw people in to Quora. Yes, the question may be the ‘search terms’, but it’s not why people end up on Quora. The question leads people in, it’s the ANSWER that keeps them there. It’s the answers that people spend their time reading, not the questions.

This is the iceberg that Quora doesn’t get nor do they even understand. The questions are stubs. The questions are merely the arrow pointing the way. It’s not the end, it’s the beginning. The questions are not the reason people visit Quora.

By producing the Partner Program, Quora has flipped the answer authors the proverbial middle finger.![]() If you’re a Quora answer author, you should definitely consider the Partner Program as insulting. Quora has effectively told the answer authors, “Your answers are worthless. Only questions have monetary value.” Yes, let’s reward the question writers who’ve spent perhaps less than 5 minutes devising a sentence. Let’s completely ignore the answer authors who have spent sometimes hours or days crafting their words, researching those words for clarity and truthfulness and ensuring trust in each detailed answer.

If you’re a Quora answer author, you should definitely consider the Partner Program as insulting. Quora has effectively told the answer authors, “Your answers are worthless. Only questions have monetary value.” Yes, let’s reward the question writers who’ve spent perhaps less than 5 minutes devising a sentence. Let’s completely ignore the answer authors who have spent sometimes hours or days crafting their words, researching those words for clarity and truthfulness and ensuring trust in each detailed answer.

It’s not the questions that draw people in, Quora staff. People visit Quora for the answers. Without thoughtful answers, there is absolutely no reason to visit Quora.

Indeed, Quora’s thinking is completely backasswards, foolish and clownish. It shows just how much a clown outfit Quora really is. Seriously, placing value on the questions at the expense of answer authors who spend hours crafting detailed answers is the very definition of clownish. That situation would be synonymous to The Washington Post or The New York Times valuing and paying readers to leave comments and then asking their journalists to spend their own time and money writing and researching their articles, only to give the article to the newspaper for free. How many journalists would have ever become journalists knowing this business model?

Qlowns

Whomever at Quora dreamed up this clownish idea should be summarily walked to the door. Dissing and dismissing the very lifeblood of your site, the actual question authors, is just intensely one of the most stupid and insane things I’ve seen a site do in its life.

Not only is the very concept of the partner program qlownish, not only does it completely dissuade authors from participating in Quora, not only is it completely backwards thinking, not only does it reward question authors (which honestly makes no sense at all), this program does nothing to establish trust or indeed, does nothing to put forth any journalistic integrity.