Is DealDash a Scam?

Updated for 2023. I’ve always been fond of online auctions, until I found DealDash several years ago. I’ve also seen a number of people who have complained about DealDash and how it operates. Let’s explore if it’s a scam.

Auctions and Bidding

In a traditional auction, you’re actually buying from a seller who has put an item up for consignment to the auction house. This is how eBay works it. The seller uses the eBay platform to pay for their auction. If the item sells, eBay gets a cut of the profit. This is a typical auction from a typical auction house.

Bidders pay nothing to bid at eBay. You simply join the platform and off you go on your merry bidding way. You will pay for any auctions you win or any Buy-It-Nows you buy, but if you bid and don’t win, you pay nothing. This is important when understanding the difference between a site like eBay and DealDash.

At eBay, auctions have a finite end. If the auction closes at 6PM today, then it’s over at 6PM. Whomever was the highest bidder at 6PM is the winner of that auction.

DealDash Auctions

With DealDash, the auctions here work a bit differently. Instead of joining and bidding for free, you must pay for your bids. The bid cost can range between 12¢ and 60¢ per bid. In order to get started on DealDash, you’ll be required to pay for some initial bids. Sometimes DealDash offers bid sales for as low as 12¢ per bid.

As for the auctions themselves, they work quite a bit differently from eBay. Unlike eBay’s fixed close time, DealDash has no fixed auction close. Their auctions infinitely run and continue to extend until the 10 second countdown timer runs out without any further bids. As long as even one bid happens within that 10 second countdown, the auction extends with another 10 second countdown timer. Basically, an auction can run infinitely or until no one else places a bid. Bids also increment the item cost at 1¢ per bid. You spend 12-60 cents to raise the bid on an item by 1¢. Admittedly, that means the item cost goes up very slowly, but it also means that the bidding can go on for days with enough bidders.

Bid Extensions

You’re probably wondering about how people can manage to bid within 10 seconds. To answer your question, they don’t. Bidders use a feature that DealDash offers known as Bid Buddy. See below for more details. Suffice it to say that DealDash’s automated system continues punching in those bids in an automated way so users don’t have to. You’ll also notice that many of those bids are made right at the last moment of second 9. There’s no way a human could time a bid that precisely.

However, there has been some speculation that some of the bidding is rigged by DealDash. That speculation alleges that DealDash itself has its own set of automated bidders driving up auction prices and bringing attention to those auctions. I can’t tell one way or another if this is true. I’ll leave that speculation alone because of Bid Buddy and how it works.

Buy-It-Now

Both eBay and DealDash offer a Buy-It-Now option. However, these work entirely differently between DealDash and eBay. The eBay Buy-It-Now feature can be standalone or attached to an auction. If it’s standalone, you can only buy that product through Buy-It-Now. If it’s attached to an auction, you can only use Buy-It-Now before the auction begins. Once an auction has a first bid, the Buy-It-Now option disappears for that item.

With DealDash, if you bid on an auction, you are eligible to Buy-It-Now when the auction finally closes. You’ll buy the item at whatever price that DealDash offers, which they claim is usually at a substantial discount. In addition to buying the item, you’ll also get all of your bids back for free. This means you can reuse those bids again on future auctions. It’s not a bad deal if you really want that item. However, if you decline the Buy-It-Now purchase, you lose all of your bids. There’s a big incentive to bid on items where you are likely to buy it when the auction closes no matter the price.

Bid Buddy

DealDash offers an automated bidding service called Bid Buddy. It continues to bid on your behalf even when you’re not around to do so. eBay also has a similar feature, but it’s tied to the actual bidding process and doesn’t have a name. If you put in your maximum bid on an eBay auction, eBay will continue to bid on your behalf at the current bid increment until your maximum bid is reached. After that, you’d be responsible for upping your maximum bid or bidding manually.

Bid Buddy works in a similar way. It continues to bid on your behalf until you’ve run out of bids or reached the maximum number of bids set on that auction. The reason to use Bid Buddy is clear. Those who are using Bid Buddy get priority over those who are manually bidding. It is in your best interest to set up and use Bid Buddy rather than manually bidding. Otherwise, your manual bid will always be last in line.

So far, So good

So far, there’s nothing here extraordinarily bad about how DealDash works. Other than the infinitely open auction which I don’t personally like, it’s pretty straightforward in how it all works.

Products and Quality

Here’s where this site falls down hard. Do you go to DealDash to buy merchandise for a great deal or to spend time gambling to win? If it’s the former reason, then you might run into problems considering all of the below. If it’s for the latter reason, you might want to seek gambling help.

DealDash claims to offer overstocked products at “discount” prices. The difficulty with this business model is that DealDash is in this business to make money off of bidding with the side effect of an eventual sale of a product. They are not a retailer, not a discounter and definitely not in any way a reputable store. They are an auction house and that’s how they run it.

As a buyer, you’ll notice there’s nothing mentioned about a Return Policy or what to do if you receive damaged or unacceptable goods. Indeed, there’s nothing on any of DealDash’s auction listings that even mention the quality or authenticity of the merchandise that you will receive if you buy or win the bid.

The products purport to be genuine, but are they? Also, unlike eBay where there’s a seller behind each and every product, with DealDash, DealDash is the seller. This means that if you have a question about the sale of a product, you have to go to DealDash to get it answered. Worse, buyers have tried doing this with no response from DealDash.

If you’re actually wanting the product you’re bidding on, you might want to consider that what you’ll receive may entirely differ from the listing. In other words, the trust level with DealDash’s merchandise is very, very low. If you really want that merchandise, you can probably find it cheaper from a more reliable seller on eBay or Amazon without the bidding fees. On eBay, both the sellers and the products themselves have a reputation score. You can see what buyers are saying about both the product in the listing and of the seller’s reputation. You’ll notice that on DealDash, there is no reputation information about the seller nor reviews from buyers about the product or what they received. DealDash is a black box.

Being the black box that it is, unfortunately, DealDash is about as scammy as it can get from a site like this. If you can’t readily see what other buyers have received from a listing, then how do you know that you’ll receive anything of value? You don’t.

Additionally, because DealDash is not a traditional store, returning any merchandise may be next to impossible, particularly when you can’t get in touch with anyone at DealDash. If the item you receive is damaged, misrepresented or outright garbage, you’re stuck with it. Otherwise, you’ll have to dispute the credit card charge. The only other thing you can do is complain about DealDash… and many people have done exactly that on RipOff Report. However, other than venting your frustrations to the world or forcing a chargeback, you may not be able to get your money back.

Jumpers and No Jumper Auctions

Here’s where DealDash also gets just a little bit more scammy with their auction site piece. A jumper is a person who jumps in at the last minute and begins bidding on an auction when they think the auction time is about to run out. Unfortunately, jumpers on DealDash effectively mean nothing. A “No Jumper Auction” is simply a way to allow early bidders not to be outbid by someone who wants to jump in at the last minute. With DealDash, there is no such thing as a ‘last minute’. On eBay, there is a ‘last minute’ because auctions have a hard close time. On DealDash, the auction is infinitely extended so long as even one person continues bidding.

A “No Jumper Auction” sets a minimum bid point that after that no new bidders are allowed to enter the auction. If the no jumper point is set to $5, that means new bidders attempting to bid after $5 will be unable to do so. Only bidders who placed at least one bid below $5 will be able to continue bidding on that auction.

This then excludes users from auctions after the no jumper bid price has been met. On eBay, this is called ‘sniping’ or ‘snipers’. A sniper is a little different from a jumper in that because the auction close time is finite, snipers join in during the last 30 second countdown to try and outbid the current high bidder. With DealDash, a “No Jumper” feature is entirely pointless and just gives DealDash a way to manipulate auctions and who can bid. This feature only serves to force people into auctions early or wait for another one to start. This feature is simply a way to lower competition and allow early birds to win the auction more quickly without extra folks jumping in and keeping the auction open much longer. That seems to go against the idea of DealDash making more money. It’s kind of a weird feature for DealDash to add such a limit to their auctions and prevent even more bidding, losing DealDash even more money in this process. As I said, it’s weird.

The scammy part of this is that apparently these “No Jumper” auctions don’t work properly, or DealDash is able to manipulate the “No Jumper” price randomly against would-be bidders. Some bidders have claimed to join in on standard “No Jumper” auctions with the default threshold set to $5. Yet, the auction price never reached $5 and they were unable to bid with DealDash claiming they were a jumper. Fishy. It seems this feature is being manipulated by DealDash in a way that prevents certain bidders (new or not) from bidding on that “No Jumper” auction.

Is DealDash worth it?

DealDash is ultimately an addictive form of legalized gambling, but it actually feels much like playing slot machines in Vegas. Mostly you lose, rarely you win and you spend a lot of money doing it…. which is how DealDash likes it. It’s what keeps them in business. If you’re willing to Buy-It-Now, you can buy back some of your bids at the cost of the product stated in the listing. But, don’t expect the price of the Buy-It-Now merchandise to be any less expensive than what you’ll find in a retail store, according to many who have done this.

Some complainants who’ve used the Buy-It-Now option have been quite disappointed in the process. One user claimed that instead of getting their bids back as promised, the “total value” of the bids was deducted from the price of the Buy-It-Now item. However, the “total value” of the bids applied to the reduction in the item’s cost were substantially lower than what the user paid for the actual bids. They might deduct at 12¢ per bid when the user paid 60¢ for the bids. Assuming you can actually get your bids back instead of this deduction thing, that’ll buy you a little more time to bid on new items and addict you further to this form of legalized gambling. This getting-bids-back idea is a little like losing $500 at BlackJack and then winning back $100. You’ve still lost $400. It’s simply a way to make you feel a little better about having lost $400 instead of $500.

If you get a high off of gambling, DealDash may be worth it… particularly if you don’t care about whatever it is you might win.

If you do happen to win the bid on item, then you’ll lose all of your bids plus whatever the winning cost of the item. If you happen to win a bundle of bids, then you’ll lose your bids only to gain some back. If you win the bid on a pair of earrings, you’ve lost however many bids it took to win that bid plus the cost of those earrings.

Consider if you don’t do Buy-It-Now often and you continually keep losing bids, you need to keep track of how much money you’ve spent there. You need to keep track because all of your lost bid money adds up when you finally do win a bid. For example, if you’ve spent $500 buying and losing bids for a while, then win a $50 coffeemaker, technically you’ve spent $550 for that coffeemaker. That’s not such a great deal. You could have bought 11 coffeemakers for the amount of money you spent to win that bid at DealDash. You simply can’t ignore all of the money you’ve spent on bids as non-existent. Those bid costs add into the cost of any items you bid and win. This means you can’t claim you got a toaster for $5. It was $5 plus the cost of however many bids it took you to get there.

Scam or Not?

The idea behind the site is fine, the execution of it is poor. If DealDash had partnered with legitimate sellers to back each of the auction products and if DealDash had allowed buyers to review the product listings for quality and authenticity and if DealDash offered a buyer’s protection plan and an actual Return Policy like a legitimate store, I might be more inclined to say it’s not a scam.

As it is, because DealDash doesn’t act like a legitimate store and also doesn’t offer feedback from buyers nor is there a buyer and seller relationship to ask questions, I cannot recommend the use of this site for any purpose… not for buying products and definitely not for getting a gambling fix.

There’s too much of a chance to lose far too much bid money and very slim chances you’ll actually win a bid. Of course, you’ll be given the option to Buy-It-Now and get your bids back on auctions where you lost the bids, but that’s of little consolation if the merchandise you receive is trash, assuming you receive anything at all. Between the bids you pay for and the Buy-It-Now, this is how DealDash makes money. The rest is all an addictive game.

Testimonials in TV Ads

DealDash has been recently running heavy TV advertising for their site in 2023. Don’t be fooled by those advertisement folks holding up a piece of merchandise that they claim to have received from winning an auction at some insanely low price. There’s no guarantee those “winners” are legitimate. You also have no idea if the merchandise received is legitimate, counterfeit, refurbished, used, hot or in any other condition.

Even if the “winners” are legitimate and not just staged by actors, you don’t know how much those people actually spent in buying DealDash bids over many months or years to “win” the privilege of buying that item at that price. They could have been bidding for years and may have already spent a ton on bids before they finally won that iPad for $35. In fact, they could very well have spent more money in bids + cost of product than simply going to the Apple store and paying full price for an iPad. Even then, when buying from the Apple store, you know you’ve purchased a legitimate iPad backed by an official Apple return policy. Getting that same device from DealDash, you don’t know what you might get; it could even be an old generation iPad from years ago.

DealDash is just like being in a Casino. When you hear the bells ring and see the lights flash on a machine because someone has hit the jackpot, you really don’t know if that’s a true win or if someone is simply making back a little money towards money they’ve already lost.

Recommendation

Site Recommendation: 👎 Avoid!

Reasons:

- Highly Addictive

- Form of gambling

- Not a store

- No Return Policy listed

- No Product Reviews

- No User Reviews

- No Seller Reviews

- Auction items don’t describe authenticity or condition

- Pay to bid

- Pay to win (separate from item cost)

- Costly

- Difficult to Communicate with DealDash

- Mostly a scam to separate you from your money

- Doesn’t operate like a legitimate store

- May be less costly to shop elsewhere

- Questionable business practices

The bottom line is, DealDash has a very scammy business model.

As always, if you find Randocity a fascinating read, please leave a comment below and please click the Follow button in the upper right under the Search bar to be notified of any new Randocity articles.

↩︎

Investor Alert: Is Masterworks.io a scam?

Every once in a while, someone decides to sell shares in “something” new. Today, that something is Fine Art. Let’s explore the pitfalls of investing in this idea.

Investing in Art

Purchasing art has always been about buying a single piece of artwork outright. Meaning, you find a piece of art you like and you buy it. That means that piece of art is yours to display in any way you wish. This type of purchasing of art is (and remains) the most optimal way to purchase art. You buy it outright and you own the entire work in totality.

However, there are exceptions to the above. If you purchase a reproduction of an original work of art, this purchase offers much fewer rights to the buyer. Some rights that you forfeit when purchasing a reproduction include reproduction of that art. Meaning, you can display your purchase in any way you choose, but you cannot photograph it and/or sell photographs of that art. The reproduction rights remain with the original work’s owner. Only the person who owns the original artwork may reproduce the work in any way.

Mass Produced

You may be thinking, “But, mine is painted with real paint on real canvas”. That doesn’t matter. What matters is if the painting is the first and the original. Many painters reproduce their works using paint on canvas, many times over. Typically, these reproduction paintings are painted by employees (in a sort of paint-by-number situation), but is not always painted by the original artist. These are painters hired for the sole purpose of creating a copy of the original. These reproduction paintings are sold typically at a fraction of the original art’s cost. These reproductions rarely become valuable simply because of the total number produced. It’s the same reason why many mass produced items rarely go up in value.

Because the original was painted by the actual artist, this original painting is the one that holds value. That’s not to say that every original painting by every artist will increase in value. Many do not. It depends on the artist, the artwork and that artist’s contribution to the art world. Perhaps in time that artist might be seen in some kind of historical light, thus propelling their artwork values upward.

Because an original art piece might spawn many “authorized” copies, copies that could become very popular in sales, that makes the original work much more valuable. For example, an original Thomas Kinkade painting would be worth far more than one of its many reproductions. That doesn’t mean reproductions can’t increase in value, but they will never be valued the same as the original first painting.

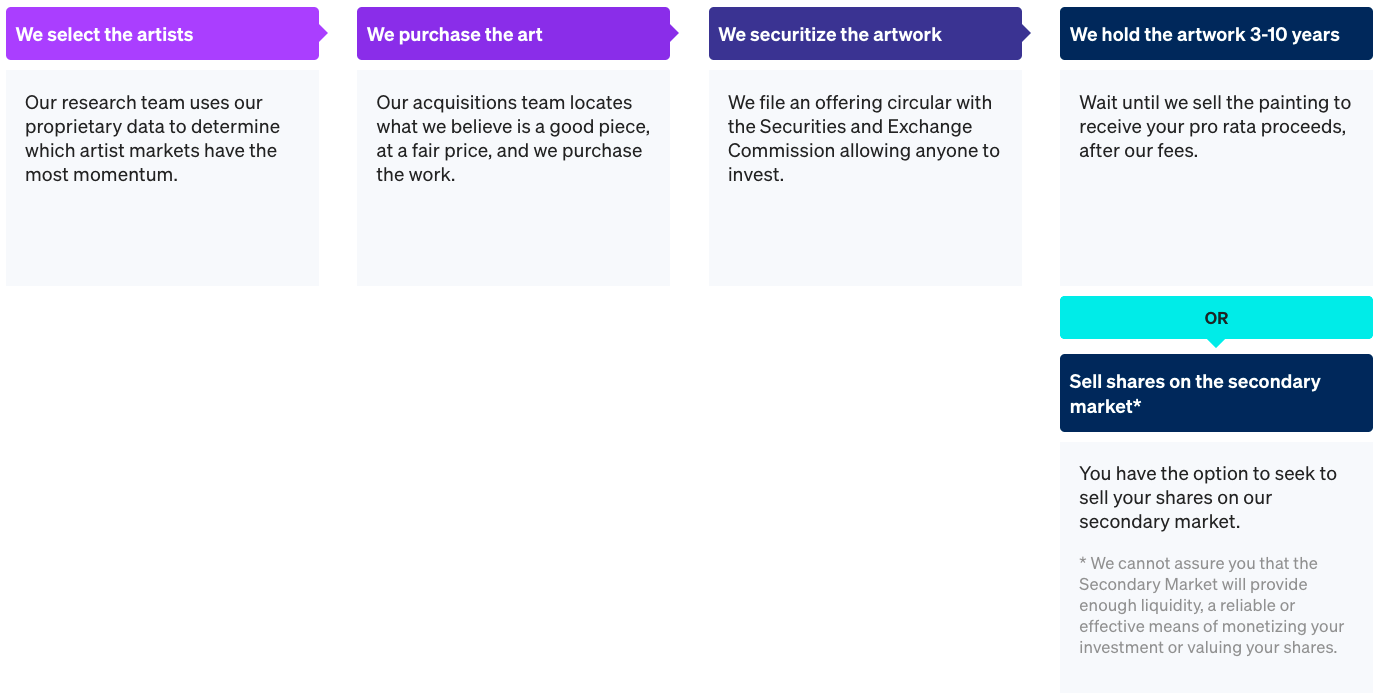

Masterworks.io

Masterworks takes the idea of Fine Art to an “investment” level. By that I mean instead of owning the actual painting / art piece in full, you only own a “share” (or small portion) of the art. In reality, this type of investing is an abstract concept. At the moment, Masterworks appears to focus solely on paintings. You might be wondering, “How does owning a small piece of a whole actually work?”

The short answer to this question is that it doesn’t. Investing in a tiny piece of a valuable work of art doesn’t do anything but ultimately make Masterworks as a company rich. You, in fact, don’t own anything but the knowledge that you “might” own a small piece of a work of art. You also own the knowledge that that investment might, maybe return value IF the painting is (eventually or ever) sold at a profit. In essence, you’re essentially placing a long shot bet that eventually that painting might be sold for a profit.

Let’s understand some of the problems with this idea.

Where is that painting?

Good question. If you’re buying into an investment object, you definitely want / need to know exactly where that “object” is physically located in the world. If you invest in a company, for example, you know where their headquarters are. You know who their executives are. You know their physical address and phone number. You can call and talk to someone. You can even find out their sales plans, the products or services the company sells and how much they make in revenue per quarter. Keep in mind that some private companies may be unwilling to disclose their sales numbers. With public companies, that company’s revenues are public knowledge.

Buying into a Masterworks painting, on the other hand, you don’t know exactly where it is. You don’t know under what conditions it’s being stored. You don’t know who currently has possession of it. Masterworks can “assure” you that that item is safe… but is it? Paintings are particularly susceptible to deterioration if not kept under the strictest of environmental controls. Artwork is also susceptible to theft. Both of these issues are difficult to manage at the best of times.

One might think that paying to invest in small bit of a painting might help protect it from being lost to time. It’s a lofty ideal. It’s, unfortunately, an ideal that when considering the underlying logistics of it all, make the investment seem highly risky. It’s also an ideal that may not hold true.

An investor should always ask, “Who owns the original work?” You must also consider the following:

- Is Masterworks attempting to sell shares in art they don’t legally own?

- Is Masterworks actually in possession of the art they claim to have bought?

- Did Masterworks actually buy the painting or is it under some kind of “lease”?

- Is the art being stored in correct conditions?

Who knows for sure? These are all very good questions. They’re also questions that should greatly concern you when considering “investing” in art through Masterworks.

Paintings as Investments

Art is entirely subjective to every person, but it is also highly volatile in its salability. What I mean is that paintings, particularly abstract paintings, go through ebbs and flows, waxing and waning in popularity and, yes, value. What might seem like an excellent painting today may be seen as outdated and worthless next year. Art’s value comes and goes, sometimes as a result of changing style trends. Painting values are, as I’ve said above, highly volatile. Way more volatile than investing in company stocks, bonds or even precious metals.

Sure, this investment type is yet another “thing” you can put some money into as part of your larger investment portfolio and hope to see a return on investment, but it may not return anything. The problematic issue with this concept is, can Masterworks be trusted or are they simply another Bernie Madoff? This is the ultimate question.

Novel Concept, Poorly Realized

The idea of share investing in art is definitely novel, even Masterworks states as much. However, is it realistic?

First, there’s the idea that you only own a tiny fraction of a painting. How does that work anyway? Are they planning on cutting up the piece of art if the art price bottoms out and there’s nothing left to pay you back your investment? Clearly, no. They’re simply going to tell you that you’re out your money and they STILL get to keep that art even if it’s worthless. Not only do you NOT get the art after investing, you don’t get your investment back if the painting is sold at a loss.

Second, there’s the logistics of where this art is stored. You have no idea as an investor. Unless Masterworks intends to spend boatloads to create a location to store all of this art under perfect archival environmental conditions (highly unlikely) AND they can prove that fact to investors, the art is then completely open to deterioration, decay and possibly destruction or even theft. Some art, in fact, may be produced using non-archival media. This means that no matter how well a piece of art is stored, it may still slowly (or quickly) deteriorate to the point of no longer even being art (or saleable) even within a few months. You can’t stop deterioration, which actually makes some art less valuable every day that passes.

Third, who actually owns (and holds) that art? Are art owners selling the full piece of art, selling it under consignment or are they selling only the concept of ownership as shares, so then Masterworks then manages that “concept trust”? If Masterworks is selling shares in works of art they do not rightfully own and possess, that is very close to a Ponzi scheme. It may also be very illegal. That’s like someone claiming to sell you the Brooklyn Bridge. Sure, anyone can claim to sell it, but they do not own it. They do not even own a piece of it. Giving money to someone claiming to sell you the Brooklyn Bridge is, thus, the very definition of a scam and fraud. With Masterworks, be very careful.

Masterworks needs to also be very careful in what they are doing, making sure their ‘i’s are all dotted and their ‘T’s are all crossed.. Here’s what Masterworks has to say about their own model and art investing:

‣ We have a novel and unproven business model.

https://www.masterworks.io/

‣ Masterworks issuers do not expect to generate revenue, so investors will only recognize a return on their investment if the painting is eventually sold at a profit

‣ No market exists for the shares and paintings are highly illiquid, so you must be prepared to hold your investment for an indefinite period.

‣ Each Issuer owns a single painting and this lack of diversification magnifies risk.

‣ Your ability to trade or sell your shares is highly uncertain.

‣ Paintings may be sold at a loss.

‣ Costs will diminish returns.

‣ Investing in art is subject to numerous risks, including (i) claims with respect to authenticity or provenance, (ii) physical damage, (iii) legal challenges to ownership, (iv) market risks, (v) economic risks and (vi) fraud.

‣ Issuers are totally reliant on Masterworks.

‣ Masterworks has potential conflicts of interest.

‣ Timing of sale of a painting is uncertain.

None of the above (or even their web site) describes how or where the art is actually stored or maintained. It almost solely discusses the risks of investing. The fact that Masterworks also finds the need to call out that purchased shares are “illiquid” says a great deal here. This word means that there are few participants, thus low volume, which ultimately means a very low chance of ever being able to sell out of purchased shares.

Consider stocks and bonds. You can likely sell out of any of these positions in about a day. With Masterworks investments, the low volume and few participants means once you invest, you’re likely stuck holding onto that investment until the painting either sells (at a loss or profit) or fails to sell at all. Masterworks doesn’t really state what happens if you can’t sell your position with a painting that never sells. I guess you’re ultimately out your investment money.

Art Storage

As with any artwork and has been stated above, it’s important to understand how and where the art is stored and who actually owns the art. None of this is explicitly stated on Masterworks’s site. I’m actually taken aback by the fact that for all the deluge of investing information provided, there’s equivalently a severe lack of information regarding the artwork itself, where it’s stored, how it’s managed or who owns it while it’s being held for shares. That’s a big, nay HUGE, problem in my book.

However, Masterworks does say this…

What this ultimately says is that Masterworks locates and purchases art. It doesn’t exactly state what “purchase the work” actually means. Are they taking possession of the work or are they leaving it at the gallery where they found it to remain on sale? They do claim to hold a work of art for 3-10 years. I’m uncertain how this works exactly considering the second half of that “OR” statement. Only questions, few answers.

As I said, for as much information as there is about risk of investing, there’s equally as little about the actual artwork itself… which is huge red flag 🚩.

Any business straddling both the art world and the finance world should be, at once, both engaged in explaining how and where the art is to be stored and handled, but also able to explain the risks of investing. Clearly, Masterworks is only interested in documenting half of this equation.

Volume Investing

Masterworks hopes that as more people jump on board with their share idea and begin investing, a larger and higher volume share marketplace will eventually emerge to allow for easier share trading. At this moment, however, Masterworks has stated that any position you buy is likely to be “illiquid”, thus implying that this is a new market with limited options for selling shares.

In other words, if you invest $100 into a painting and gain 2 shares, those shares in that painting are most likely to remain yours until the painting sells at a profit or a loss. The question is, though, even if the painting sells, does Masterworks have the painting to sell? I’m still skeptical.

Art Galleries

Masterworks, as a company, needs to be a whole lot more forthcoming about all aspects of its business operations, especially surrounding where, how and who stores the art after it’s purchased.

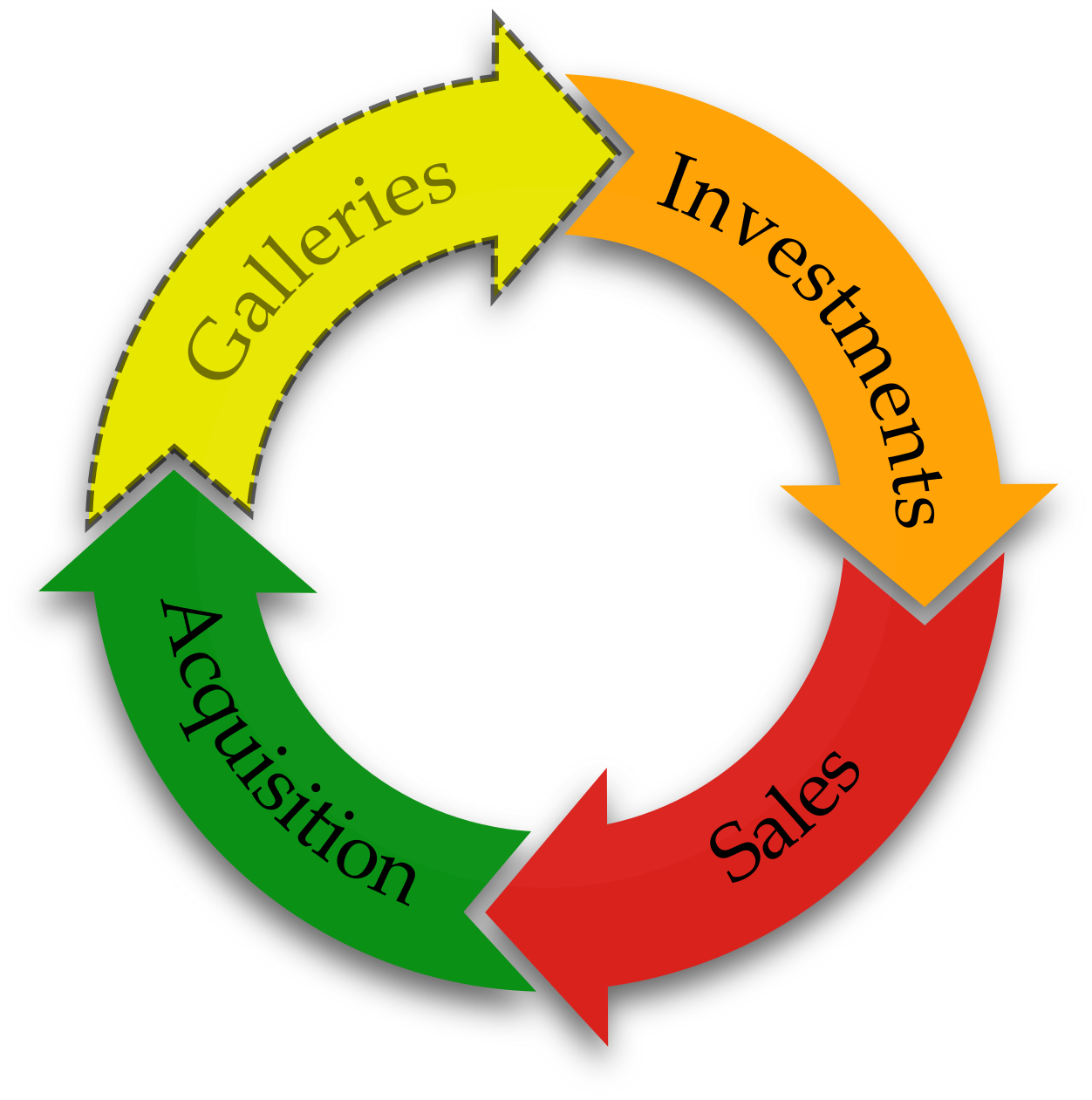

What Masterworks should have planned for is purchasing a number of galleries around the United States (or around the World) to support their business model. Instead of simply attempting to sell the investment share idea, they should have worked this idea full circle.

Here’s where things get a little dicey for Masterworks. Instead of creating a complete sales cycle (or sales funnel as some might call also it), they leave out one very important piece: Galleries. Clearly, they have Acquisition, Investments and Sales. Though, questions about Masterworks’s acquisition process remains, primarily because they don’t have galleries.

To really make this business model complete, Masterworks needs to own and operate its own set of galleries. Why galleries? Owning galleries sets a tone that you know how to properly store and manage expensive artwork in addition to offering a place to actually sell it properly. Though, paintings can be sold through auction houses as well. Masterworks is attempting to sell art for millions of dollars, yet Masterworks doesn’t really state where, or more specifically how, that artwork is managed and stored. It’s an important and necessary piece that’s conveniently missing.

Owning galleries keeps Masterworks honest and allows for auditing. If there is a gallery where a specific investment work lives, investors can visit the gallery and physically see the art they have invested in. This verifies that the artwork exists, that it is genuine (not faked), that it’s in Masterworks’s possession and that it can be verified. Without this piece, verification of the actual art remains an open question. Images on a web site do not verify that anything is genuine. Talking to someone on the phone doesn’t verify authenticity either. Only physically seeing the artwork in person can an investor verify the painting and, thus, verify that their investment is backed by something real.

Questions without Answers

That leaves too many open questions. Questions like, “What exactly am I investing in?” Like, “Where is the artwork stored?” Questions like, “Is the artwork properly stored for a long sales wait?” Like, “Is the artwork in the possession of Masterworks directly?” All of these questions could be easily resolved if Masterworks owns and operates a set of galleries… or at least a showroom at the bare minimum.

Additionally, with Masterworks ownership of galleries, this means you, as an investor, can physically go see the art you’ve invested in. You can see if it’s as it appears in the images. You can see it on exhibit, or at least it can be brought out for a viewing. You can see that it’s being kept and stored in appropriate environmental conditions.

There are so many questions surrounding the art itself, there is absolutely no way I would recommend anyone to invest in Masterworks… unless you absolutely like throwing money away on odd “investment” strategies. Knowing where that art is, how it’s being stored and if it’s being stored appropriately combined with knowing you’re able to view the actual art is extremely important BEFORE investing any money in a share of a painting.

Ponzi Scheme?

While I previously made reference to Bernie Madoff and his ponzi scheme, that statement isn’t intended to suggest that Masterworks runs a Ponzi scheme or that it intends to make off with your money. However, because of so many lingering questions, this business model seems unnecessarily risky… especially not knowing the answer to far too many questions surrounding the paintings.

Additionally, because of the volatility in art sales, as an investor, you must fully trust and be reliant on Masterworks buyers and appraisers to locate “valuable art” that might sell for some amount of money higher than what was paid. However, you’ve no idea if the art they’ve selected will actually sell at all. Because art is so subjective, what a few like, too many others may hate.

It also means betting that some nebulous “whale” will come along and snap up that piece of art (for millions) you just so happen to have invested in. That isn’t likely to happen often. Unless the art is of great historical value (i.e., Leonardo DaVinci or Michaelangelo or even more recent artists like Mark Rothko, Roy Lichtenstein or Marcel Duchamp), art produced by artists living and working today might fetch random amounts, but perhaps not millions. There’s just no way to know what any piece of art might fetch when produced by today’s artists. It’s all a calculated, but a seriously risky best guess.

Unfair to Artists

One thing Masterworks also seems to be attempting is to force art to be sold at far higher prices than it’s actually worth. This is what many collectors attempt to do, usually via auction. That is, Masterworks appears to intend to artificially inflate art prices to make better returns on shareholder investments. The difficulty is that this artificial inflation (nor does the sale itself) benefit the artist at all.

Where Masterworks might “buy” a work for $70,000 from an artist via a gallery, they may attempt to turn it for $1.3 million. That nets a huge profit for Masterworks and a lesser amount for shareholders in that work. However, for the artist, $70k is all they have received. The artist is not fairly compensated from a Masterworks sale.

One might argue that aftermarket sales of art never has benefited the artist. Yes, but here’s a business model that could arguably help bring artists into the fold by making sales on behalf of the artist. This goes hand-in-hand in owning galleries. Instead, it seems Masterworks has chosen an aftermarket sales model that excludes the artist. A model that only makes money for investors and Masterworks, but not for the artist. Intentionally leaving the artist out of this process is entirely greedy and unfair to the artist.

Artists Deserve Compensation

One might think that $70,000 is a lot of money for the sale of a painting. It is. But, it is nowhere near the amount that the artist could have netted if they had sold it for $1.3 million.

Artists shouldn’t be required to invest in their own paintings with Masterworks just to net more profit on an aftermarket sale. Instead, Masterworks should work directly with artists to list the work and then compensate the artist for at least 50% of the sale, either directly or by issuing a 50% ownership stake in the art via shares. The rest of the profits should go to paying out shareholders. This model would not only fairly compensate every artist, but it also fairly compensates the shareholders and Masterworks itself.

Artists are always the one who seem to get the shaft. This problem has existed for many, many years. Masterworks can modify their business model to make sales that directly benefit the artist while also properly compensating shareholders and turning a nice profit for Masterworks. Instead, it seems they have ignored this aspect only to make their sales benefit mostly Masterworks executives the most, leaving out the artist.

Artists vs Corporations

If you’re of the mindset that you would like to see artists fairly compensated for their work, skip these risky investment schemes and buy directly from an artist. If you buy directly from an artist, you are helping that artist, not some random corporate executives operating a more or less faceless and questionable company. If you’re willing to shell out $20 to see a movie actor perform, then why wouldn’t you be willing to pay an artist for the artwork they produce?

Not only can you carry pride in the fact that you purchased art directly from the artist, you also own an original work of art in full, not solely just a share in a work of art that you’ll never see. You can also hold pride in knowing that you have helped the artist produce even more work. Buying art from Masterworks does not, in any way, encourage artists to continue to their craft. In fact, the pittance that the artist might receive in the first sale may be barely enough to cover the time and effort put into producing that painting let alone help them produce future paintings. Art supplies are expensive.

Art Valuation and Secondary Market

Let’s talk about the investing and trading pieces. Masterworks operates a secondary market where shares can be traded. Unlike Wall Street stocks where a stock’s value is based on such fluctuating data points as company profits, company revenue, investor calls, product sales and announcements, analyst recommendations, investor confidence and volume of trading, paintings have no such intrinsic back end data points (other than perhaps trading volume… and even that is drummed up via this questionable investment scheme).

Art valuation is entirely subjective, made solely by a random person appraising its value. What that means is that if you invest in a work that claims to have a $30 “share price”, you’re at the mercy of an appraiser to raise or lower this price. Bid and ask sale prices might influence pricing some, but the pricing seen on the secondary market site is mostly “best guess”. There’s nothing behind that painting to “prop up” its changing value. There are no profit margins, no new product announcements, no analyst calls, no company books to review, nothing. It’s a painting. That’s it. Paintings don’t randomly change value UNLESS they are sold. Anything else purported is a dubious scheme.

Investing in a painting with a fluctuating value is a false equivalence to stock. There’s nothing there to change the value of the share in a painting, yet it seems that the values do change. Why? The painting hasn’t yet sold, so it makes zero sense. As I said, there’s nothing in any painting to justify changes in the share price until AFTER it’s sold. Once a painting has been sold, then the share price will change to reflect the sale price of the painting.

If Masterworks intends to see a painting’s share price fluctuate daily, like stocks, then there’s something seedy, dubious and awry going on. It’s also something that you as an investor need to understand before investing a cent. Intraday changes in painting’s share price prior to a sale is extremely dubious.

One might argue that there are a limited number of shares in the painting. That each share sold makes every share more valuable. I might be willing to accept that argument except a painting can be arbitrarily divided 100 times, 1,000 times or even 1 million times. When does that share division end? You can’t really divide a painting up like that. If you’re going to apply a random investment concept, such as a share, onto a painting, then any division into shares is entirely arbitrary and disconnected and holds effectively a fractional value tied to the current “worth” of the painting. Ultimately, there’s only one (1) painting. Therefore, there should only be one (1) share. When you buy that one (1) share, you buy the painting.

Having this sub-construct of many shares which are separate from the “painting as a single commodity” is not only an odd concept to apply to a physical object, it might be seen as a form of Ponzi scheme. These “shares” are actually an abstract idea applied to a single physical object which cannot be subdivided physically. So, how exactly does this abstract division concept work? That’s exactly what Masterworks is attempting to find out. It’s also why the Masterworks business model is unproven.

Overall

I can’t recommend investing “shares” in paintings via Masterworks for reasons already outlined above. However, let me summarize these points:

- Proper art storage isn’t explained (very high risk)

- Returns on investment isn’t fully explained (high risk)

- Paintings aren’t guaranteed to sell (high risk)

- No sales benefits given to the artist (problematic)

- No galleries to physically view or confirm ownership (exceedingly high risk)

- Art prices are highly volatile (high risk)

- Art sales are solely dependent on subjective criteria (overly risky)

- Art values are solely dependent on Masterworks “appraisers” (highly risky, requires high trust)

- Intraday changes in share prices are nonsensical prior to the painting being sold (dubious)

- Must trust Masterworks for both valuation and truth (overly risky)

- Must trust Masterworks that they actually own and possess the art (exceedingly risky)

- Secondary market attempts to treat shares in a painting like stocks (exceedingly risky & dubious)

Without seeing the painting physically, as an investor, you have no idea if Masterworks truly has that painting in their possession. It’s easy to take a picture and put it on a web site, making claims that they own and possess the work. This then tricks the investor into a purchase. Then, you hold and hold and hold and the painting never sells. In fact, you could come to find they don’t even own the original art. You might find that they’re selling something they don’t even have possession of.

While Masterworks may own some of the work they claim to own, there’s literally no way for an investor to confirm that every piece of art listed is actually in the possession of Masterworks. This problem is exacerbated mainly because Masterworks operate no galleries.

For this reason, Masterworks could be selling you shares in a work that they do not, in fact, own or possess. That’s effectively a form of fraud.

Masterworks would do best to modify their business model to offer a process that can prove they physically own the paintings they claim to own. The only way this is really possible is if they open and operate at least one Masterworks gallery somewhere so shareholders can visit and request a viewing of the art they’ve invested in. This is effectively an audit system which holds Masterworks accountable to all shareholders. Without this change in their business model, investing in any work that Masterwork claims to own is unnecessarily risky. To anyone willing to give money to this company, I say, “caveat emptor!” Let the buyer beware.

Without such basic investor auditing responsibilities, I strongly recommend staying away from this novel, but highly problematic investing concept and stay away from Masterworks as a corporation. That’s not to say this concept can’t be revised to be more functional, but at the moment this concept is just not there. This concept forces an over-burdensome amount of trust and risk onto the investor and off of Masterworks, while leaving too many unregulated, unauditable and manipulable pieces in the hands of Masterworks executives.

Bottom Line: If an employee at Masterworks wished to game the Masterworks system, the lack of proper auditing over this concept would allow any executive far too easy access to game it… thus losing investments from investors and truly turning this into a huge fraud scheme.

Business Concept: B

Business Execution: F+

Scam Risk Level: Exceedingly High, Stay Away

Recommendation: Don’t Invest in Masterworks

↩︎

How does Twitter Philanthropy work?

How does all of this Twitter philanthropy actually work? Let’s explore the seedier side of it.

Twitter Philanthropy Exposed

I won’t name any specific accounts simply because there are too many of these accounts preying on people’s needs, but let me expose how these accounts REALLY work. There is one on top of this pile, but I will let you find it yourself. If you search Google for the key words “Twitter Philanthropy“, you will find this specific Twitter account within the first 10 search results. But, don’t go run over there just yet to follow it before reading this article.

Twitter Impersonation

Let’s start this out by explaining how these accounts operate. While some of these large Twitter philanthropy accounts purport to be operated by a single individual, they are not. Instead, they are operated by a team of individuals who have access to this single Twitter account so named for a single person. In fact, this situation is in violation of Twitter’s Terms of Service rules of impersonation.

Impersonation is a violation of the Twitter Rules. Twitter accounts that pose as another person, brand, or organization in a confusing or deceptive manner may be permanently suspended under Twitter’s impersonation policy.

By operating an account as a team, rather than by the single individual named on the account, this is definitely impersonation… regardless of whether the single individual has authorized that “team” for that purpose.

If you are interacting with a Twitter account who appears to be a single person, but unbeknownst to you there are actually multiple people who are not the named individual operating that account, this is entirely deceptive and misleading… and the very definition of impersonation. You are not dealing with the person you think you are. This is in violation of Twitter’s rules. Whether Twitter sees it that way is entirely subjective and based on Twitter’s whims, unfortunately.

Team Accounts

There are many team operated accounts on Twitter. Many celebrities operate such accounts. Since the celeb can’t be at the account 24/7 to answer responses, they hire staff to manage these tweets. Most times, these celebrities are represented fairly and appropriately by their hired staff, mostly because the staffers remain in close contact with the celebrity to make sure the tweets are appropriate to the celebrity’s brand.

With these philanthropy accounts, it seems these are much more loosely operated. The team is made up of people around Twitter who manage this account and have Twitter accounts of their own. They don’t always seem to have direct approval of the account owner. If you read through some of these philanthropic account tweets, they seem to show random and incoherent tweet-to-tweet messaging, espousing differing and hypocritical ideals. Why? Because different people are posting these tweets to that single account under the guise of impersonating a single person.

Philanthropy Exposed

While these accounts may have started out as genuine philanthropy, they have degraded into an odd scam that takes advantage of people’s needs… and mostly exist as ways of gaining followers. Worse, these accounts breed even more scam artists. Scam artists who WILL take advantage of you and scam you in the process. I’ll talk about the scammers at the end and how those work. Let’s focus on the actual purported philanthropy accounts first.

Why a team?

Good question and one that you’ll understand once I explain it. Basically, when more team staffers are attempting to locate money from other contributors, that means more money to share in the guise of philanthropy under that single Twitter account. Looking for contributions isn’t the problem here, though. It’s the scammy WAY that this team goes about looking for contribution money. If this single aspect doesn’t leave a bad taste in your mouth, keep following along as it gets so much worse.

The team that makes up the single top Twitter philanthropy account uses Twitter (and sites like GoFundMe) to gain money first. Instead of actually giving out money from the purported account owner, the team actually solicits money contributions from random people using dubious methods including begging, groveling and outright scamming using sites like GoFundMe. These team members are then adding their ill-gotten money into that Twitter account’s philanthropy fund for giveaways.

Here’s where the deceptive part comes in. This team of people collect these monies using their own personal accounts, accounts not associated with that Twitter philanthropy account. This makes it difficult to trace where that philanthropy money actually came from. Deceptive and a form of money laundering. Dirty. When other people contribute their money to one of these outside accounts for some possibly even fake purported need, this is a huge problem for these larger philanthropist accounts. Any money given out by a philanthropist shouldn’t have been obtained by using a scam. Yet, here we are.

Yes, this means this team is not actually giving out the philanthropy account owner’s money, as is implied by the account owner’s statements. Instead, that team is raising funds using outside means, possibly using deceptive means (claiming to be raising money on behalf of a veteran or claiming to have a high electric bill). Then, they take that money that has been raised and give it out on Twitter. Do they give out 100% of that contributed money? Do they use the money towards the claimed need? My guess to both of these questions is no. These philanthropy accounts might be keeping as much as 50% or more of the money they collect and, in turn, only give out 50% or less of those ill-gotten contributed funds.

It’s one thing to solicit money for an intended purpose and use it for that purpose. It’s entirely another to solicit money for a purpose, not use it for that purpose and give it away to someone on Twitter. Full disclosure here? Yeah, no. Not to mention the tax ramifications of such a setup.

Giving Money Away

While giving away money might seem a good thing, this action actually preys on people in need. Worse, the way these accounts are being managed is dubious at best. Yes, it gets even worse. These accounts have so many followers that they can’t possibly manage what gets written into their Tweets. What you’ll find in most of the Tweet replies consist of people claiming to also give away money. I’d bet that at least 99.9% of these people dropping in Tweet replies are scammers looking to part you from your money. It might even be some of the team running that same philanthropy account looking for money for their next “giveaway”.

This is why this situation is a double whammy for those in need. Not only is there so little money given away from these top Twitter philanthropy accounts (they can only raise a couple hundred dollars at a time usually), the Tweet replies are chock full of scam artists willing to take advantage of you.

The act of giving away this money on Twitter might seem altruistic, but I guarantee you that it is not. There is no altruism going on here. It’s all about gaining followers on Twitter and making it SEEM like the account is altruistic. It’s just a show. The reality is, it’s a business that follows the following formula:

- Team hides behind Philanthropy account (unbeknownst to Twitter followers)

- Team is tasked to raise money (using whatever dubious means necessary) from random individuals, each team member raising money separately using their own individual accounts

- Team places raised money into Twitter account fund for “giveaways”

- Team likely keeps much of that money for themselves as “payment”

- Twitter Philanthropy occasionally awards random folks for random reasons

What if I win?

If you are one of the very few who manage to get picked to receive money from a philanthropic Twitter account, don’t think it’s all roses. To receive any money, you are required to jump through legal hoops before that money is deposited into your account.

“What legal hoops?”, you ask. Good question. You are required to agree to a long, stringent set of terms and conditions before you are awarded any money. These conditions allow this Twitter philanthropy account to do whatever they want with your win while restricting you. What document would I sign? You will need to read and sign a Non-Disclosure Agreement (NDA) and return it to the team operating the philanthropic account before you can take possession of that $20 or whatever small amount they are willing to give you. This is the very definition of victimizing someone in need. Someone in desperate need of money would be willing to sign just about ANYTHING to get that “free” money.

Once you agree to their restrictive terms and conditions, they will send you that money via CashApp or whatever other agreed upon payment system. If you violate these terms, they will sue you.

This is not a no-strings-attached way to get money. In fact, it wouldn’t surprise me to find that some of these “charity acts” might actually be loans which must be repaid at some point in the future. In other words, be very, very careful if you choose to attempt to get money out of these philanthropic accounts. They may screw you on the way in and on the way out… and perhaps even later in the future.

Twitter’s Response

Unfortunately, Twitter (the company) doesn’t monitor or manage any of these philanthropy accounts. They allow them to operate with impunity. Because it seems that these philanthropic accounts “appear” (it’s all about appearances) to be doing good for the community, Twitter (the company run by Jack Dorsey) turns a blind eye and allows this bad situation to continue and fester. Few people actually get anything good out of these accounts. Even more are getting scammed from the tweet replies claiming to also give away money for following and retweeting. Don’t fall for any tweet replies. They’re almost certainly a scam.

Essentially, Twitter is turning a blind eye to these accounts which, in fact, do not perform a “good service” for Twitter. In fact, there are likely more people being scammed out of their money than ever receive money from any Twitter philanthropy. On Twitter, it’s not okay to write about certain controversial topics, but it’s perfectly acceptable to take advantage of people in need and scam them out of even more money? Thanks for looking out for us, Jack!

Scams and Philanthropy

As I stated earlier about Tweet replies in the article, let’s now understand how you can get scammed through fake philanthropy on Twitter. There’s actually more fake philanthropy going on Twitter than there is genuine philanthropy.

In fact, it’s very easy to get scammed out of money on Twitter. This specific scam isn’t what the top philanthropy accounts are using, however. Instead, they use the model described above, which is nearly as seedy. With that, let’s look at how fake philanthropy accounts on Twitter attempt to part you from your money so they can sip champagne on a beach.

This next philanthropy scam is bait and switch and it’s the primary way they scam you. How this one works is that you’ll see someone Tweet replying they’re willing to give you money and all they need is your CashApp tag sent to them over a direct message (DM). You then give it to them. Seems harmless enough, right?

The Scam Begins

Over the DM area, they’ll start by asking you a lot of seemingly personal questions. If you pass all of these probing questions, they’ll explain to you that their CashApp app is broken and that they can’t use it. They’ll tell you they need to switch to using PayPal. Here’s where the scam actually begins. Any philanthropy person who switches the payment method sets up a HUGE RED 🚩. Don’t fall for this. If the person can’t use CashApp, which enticed you in, to send you the money, walk away. CashApp can be used by anyone and it can be set up quickly. Any excuse someone gives for not using CashApp is fake.

When they switch to using PayPal, they can then claim to need you to send them money to cover fees or other such nonsense to complete the PayPal cash transfer. In that goal, they’ll issue you an invoice to pay. This is the scam. First, PayPal doesn’t need money to complete a cash transfer. Anyone making this claim is scamming you. Second, you shouldn’t need to pay any money to get money. If they can legitimately pay you, they will pay you no strings attached. Third, remember that they roped you in by offering the use of CashApp, then inexplicably switched to PayPal (bait and switch).

Anyone who can legitimately pay you money can do so using CashApp. There is no need to switch to another service. You can read more about PayPal scams here, and there are plenty more just like this one.

Screenshots

To attempt to trick you further by making themselves seem legit, they will send over a screenshot showing that they paid someone else money. A screen shot is EASILY faked, let alone found on the Internet. There’s no way to verify that any screenshot they send you is in any way linked to them (or even legitimate). In other words, screenshots are not proof of anything, let alone of being charitable.

If the person is legitimate, they will send you the money without asking you for anything in return. If they ask for anything in return, it’s a scam.

Uncomfortable Questions

Other behaviors they might exhibit is asking a series of deep probing questions you might not feel comfortable answering. Specifically, question like what bank you are using, what credit card companies you have, and so on. That’s none of their business. If they’re willing to send you money under philanthropy, they don’t need any of this information. If they begin asking probing questions like social security numbers, birth dates, actual account numbers or any other deep personal information, this has the hallmark of scam all over it. Remind them that the CashApp tag is all they need to send over money. If they can’t do this simple one thing, then they’re not legitimate.

Philanthropy should be about the good in giving, not finding out as many personal details about a person as possible. If someone begins asking very deep diving personal questions about you, your location and your finances, walk away. Explain to them that they don’t need that information to be charitable. If their charity relies on this information, they can find someone else.

Chances are, the reason they are asking these personal questions is to not only scam you, but take the rest of your accounts for a ride.

The Dark Side of Twitter Philanthropy

Yes, there is actually an extremely dark side to Twitter philanthropy which has now been exposed showing just how dark it can get. No, Twitter philanthropy is not all roses, as some adamantly claim.

For a moment, let’s suppose you do win the philanthropy lottery. Let me ask you this simple question. As a recipient of that supposed good will money, do you really want to accept that money not really knowing if someone behind that philanthropy account scammed another to give you that money?

Yeah, I wouldn’t want to either. Money can be helpful, but not at the cost of someone else being scammed out of it. Be careful and tread lightly when following any Twitter philanthropy accounts. Keep your guard up and watch out for people on Twitter claiming to be altrustic do-gooders. In these especially hard times, don’t fall for fake altruism. If you are really in need of money, head over to GoFundMe and plead your own case with your money raising efforts. The money you raise at GoFundMe will be yours without such underlying strings. If you’re putting your hand out towards someone else’s wallet, particularly on Twitter, expect the worst in people.

In fact, let me point you to this exposé article describing one particular philanthropy account on Twitter. This article is a bit disjointed of a read, but if you can follow it, you will better understand this very dark and seedy side of Twitter Philanthropy in excruciating detail.

↩︎

Robocalls: Gotta Hate ‘Em

If you own a phone, you’ve likely gotten a robocall… and they suck hard. This one is short and sweet. Let’s explore.

If you own a phone, you’ve likely gotten a robocall… and they suck hard. This one is short and sweet. Let’s explore.

Most Annoying Robocall?

The most annoying robocall ever has to be this one:

“What exactly is this specific robocall all about?”, you ask?

Well, I’ll tell you! It’s a sales and marketing multi-level scam. Apparently, this scam was devised by Paul Stevenson when he formed Exitus Elite. This company sells packages of varying “educational materials” (and I use these terms loosely). These materials contain marketing and sales “education information”. Yeah, you’re selling so-called “secret knowledge” about how to make money using marketing and sales. It’s a catch-22 circular sales pitch. You’re selling the exact thing that got you roped into the scam in the first place. And, you had to pay for that “knowledge” the first time before you can actually begin selling it. Yeah… so there’s that. That’s why it’s a scam.

Most scams like this require an investment before you can begin selling the thing you got roped into buying.

Now, don’t run off and go buy into this scam lest you read the fine print details. For example, Exitus Elite offers sales of four differing “knowledge” packages priced between USD $250 and USD $1000. If it were only a one-time purchase, it might not be so bad. Unfortunately, it gets worse.

In fact, you’re actually joining a “Membership” program called “Exitus Elite” that costs $299 per year. After you pay your $299, you are hooked up to someone who can then sell you one of those four expensive “Genesis” packages priced starting at $250. Your purchase helps out the MLM “representative” you buy it from which then allows you to begin selling the very same packages to other people.

Worse, Exitus’s refund details are sketchy at best. They claim a 7 day refund policy, but good luck trying to work that out with them. Their strategy will most likely string you along past the 7 day mark and then claim it’s too late to exercise a refund (usually the reason for such short refund periods). If you try to charge the refund back to your credit card, Exitus’s terms claim the right to be able sue you. It’s actually a scare tactic. They can sue you anyway. It’s just that because you signed up by agreeing to those terms, that “agreement” may or may not hold up better in a court of law. However, no terms a company like Exitus writes can deny you your ability to use your credit card’s chargeback program. If you feel you’ve been scammed by a company, it is your right to contact your credit card company and dispute the charge.

Stay Away from MLMs advertised via Robocalls

It is always your best option is to avoid getting involved with any multi-level marketing programs, especially when they are advertised over annoying robocalls from companies which repeatedly violate the Do Not Call registry. Some MLMs may make you small amounts of money, but you’re always making money off of the backs of other people.

To succeed in an MLM, you basically have to rope people into the same MLM scheme that roped you in, forcing them to pay a lot of money to the company and giving you some tiny amount for “referral”. If you enjoy alienating friends, relatives and co-workers, then perhaps MLM money stealing scams are for you. If not, then try other more legitimate methods for making money.

If you receive this (or any) robocall that sounds similar, hang up and block the number on your phone. This action is your best option to avoid being scammed. Just forget all about that call and do something better with your time and money.

↩︎

Film Review: The Warning – PBS / Frontline Documentary

Rated: 4/5 stars.

PBS’ The Warning Documentary

The Warning is a PBS documentary discussing a warning from Brooksley Born, an attorney and a former Commodity Futures Trading Commission (CFTC) chairperson. She explained that derivatives were extremely risky insurance vehicles and sent a warning that these vehicles needed regulation during her tenure as CFTC chairperson, but her warnings went unheeded. She resigned in 1999 from the CFTC position after legislation was passed preventing her agency from regulating derivatives.

Vision of this Documentary

While I would like to rate The Warning higher, its take is pretty much tunnel vision on the derivatives markets. While the derivatives markets did melt down and did, to a large degree, spur the meltdown onward, the meltdown was not started because of derivatives. The derivative meltdown was a casualty of and was exacerbated by the sub-prime mortgage meltdown. Had the mortgage industry bubble not burst, the derivatives market might have gone unchecked for many more years. The warning was and should have been about placing regulations onto mortgage lending practices. The mortgage lending industry is the industry that failed and sent the economy into a tailspin, let’s make that perfectly clear. The derivatives (insurance) market, which speculated on the mortgage industry, single-handedly sent Wall Street into a tailspin (along with several large insurance companies like AIG).

Derivatives and the Mortgage Meltdown

Anyone with half a brain in their head could see that using questionable lending vehicles like interest only loans for the first two years or adjustable rate mortgages were ticking time bombs. When the actual monthly payments came due years later after rates went up to where they should have been, people couldn’t afford pay. This was especially true when lenders were handing these loans to people who could barely afford the ‘introductory period’ payments. So, loans came due, people defaulted and the rest is history. The derivatives (insurance policies) that were issued also came due because of the en masse foreclosures. Insurance companies that issued derivative policies speculating people wouldn’t default en masse began to fail because their speculation was wrong. So then, these insurance companies couldn’t pay off on the insurance claims. So, when consumers defaulted, so did the insurance companies offering derivatives.

It wasn’t as if warnings weren’t being issued regarding the inevitable mortgage meltdown, it’s just that Brooksley Born (the focus of this film) was not one of the people issuing the mortgage warning. Her warning was strictly about the highly risky derivatives. More specifically, the black box non-transparent nature of them. The danger, of course, is that derivatives can be placed on any speculative and risky investment as insurance. The reason derivatives need to be regulated is to prevent companies the size of AIG from making stupid decisions about such risky vehicles. However, from a consumer perspective, banks should never have gotten into the position of issuing such risky mortgages like water to people who couldn’t afford them. This was the single mistake that led to where we are today and that mistake has nothing to do with derivatives and everything to do with Government and the Federal Reserve making stupid decisions.

Overall, the movie is worth watching, but also understand its information’s place in the larger meltdown that was at work in our economy.

America’s Recession: loans and scams

Economic Downturn & The Fed

Unless you’ve been hiding in a cave, you’re probably aware that we’re going through a fairly deep recession. Recessions are cyclical, but in this case it probably could have been either avoided or lessened IF the banks and lenders had not been offering creative financing techniques. It also could likely have been avoided if our current pro-business govt. administration hadn’t chosen to look the other way while bad mortgages were being doled out. The problem with all of the creative financing is that it tended to lead some people into believing they could afford a mortgage they could not afford. When the loan reset after the promotional period, the realization quickly set in. Worse, the situation was compounded by property investors who sank huge amounts of loaned money into properties that would eventually become valued less than the loan.

It’s not as if the handwriting wasn’t on the wall several years ago when the fed dropped the rate to 1 percent. Now, we are back in this exact situation again with the fed dropping the rate to an unprecedented 1/2 percent. The feds are, again, trying to spur the economy like they did 2-3 years ago. But, this time, the banks don’t have money to lend. So, the 1/2 percent may not trickle down into the mortgage market like it did several years ago.

But, our economy is still likely being set up for yet another financial failure. The banks that do have money to lend are still advertising on the radio claiming extremely low interest rates. The problem isn’t the rate, but the loan you’ll be getting. If it’s a standard fixed rate loan, that’s fine. But, it’s the fine print you need to read. Don’t get locked into an adjustable rate mortgage or a limited time interest only loan. Once these creative loans reset in a couple of years, you may end up deep under water.

The Fed, therefore, needs to be extra careful when cutting the rates this low again to avoid the same mortgage problems all over again.

Scams in a down economy

With the economy being so depressed, it’s also a good idea to watch your money closely. As money gets tighter and tighter, the scammers will come out of the woodwork (and they already are). I’ve already noticed a drastic increase in spam and phishing emails since the economy has taken a turn. It’s going to get worse before it gets better.

There are many scams out there from the Nigerian 419 scam that claims to give you a ton of money only to rip you off of thousands of dollars before you realize it, to sending you what look like official invoices that only turn out to be scams in themselves. Don’t fall for them. The easiest way to avoid scams is to not give out any personal information to anyone who approaches you claiming to be from a legit company. This means, if you receive a call asking you to make a payment and they request for you to give a credit card over the phone, don’t. Make sure you know who this company is first and make sure you are a customer. Then, tell the company that you will call them back through their official channels and make a payment that way. As long as you are the person making the call to the official number, you should be safe. With incoming calls, you have no idea who is really calling you no matter what the CallerID says. Always, always call companies back from official numbers located on a trusted bill or from the back of your credit card.

TV advertisements that offer products or services usually employ people who are not paid very well. So, be wary when you give your credit card number out to TV commercial based purchases. Not only are some of these companies impossible to get refunds, your card number could be enrolled in a club or, worse, stolen by one of the telephone operators in an independent scam. You should always Google the product you are thinking of purchasing to 1) find out if you can find it cheaper online and 2) find out if people have had issues with either the product or the companies refund polices.

Get rich schemes are basically another form of scam. Yes, they do make someone rich… the person who created the scheme, but not you. Get rich schemes are usually designed to part you from your money. So, in a down economy, you should avoid get rich schemes (placing classified ads, setting up ecommerce sites that sell Amway products, or Multi Level Marketing – MLM schemes). Note that MLMs only make the top most people money. If you’re anywhere near the bottom, you will be parted from your money.

Craigslist and even eBay are a haven for scammers. Be careful when you work with people selling or renting things. Never buy or rent anything sight unseen and never give money out as a ‘deposit’ or to ‘hold’ something unless you truly trust the individual. Chances are, if the person you are thinking of doing business is presently outside of the US, you should immediately stop the transaction unless you know for sure that what they are selling/renting is legit.

If you are selling a car or renting out an apartment, watch out for scams here too. There are some people who are outside of the US who will claim to give you an excessive sum of money in the form of a check. They may even send you what looks like an official check.. the problem is that it will bounce causing you fees and other associated problems (and may let them get access to your account number). Don’t cash any checks like this.

The bottom line is that in this weak economy, you should be extra careful with your money as there are lots of desperate unemployed people willing to do anything to make a buck (or a thousand). Always make sure to do your homework before buying anything or giving out personal information to someone you don’t know. If you suspect a scam, you should alert your bank or credit card company immediately.

leave a comment